The acceleration in the growth of the M2 money supply in February logically leads to a decline in real GDP growth, in accordance with my law of the free money supply.

***

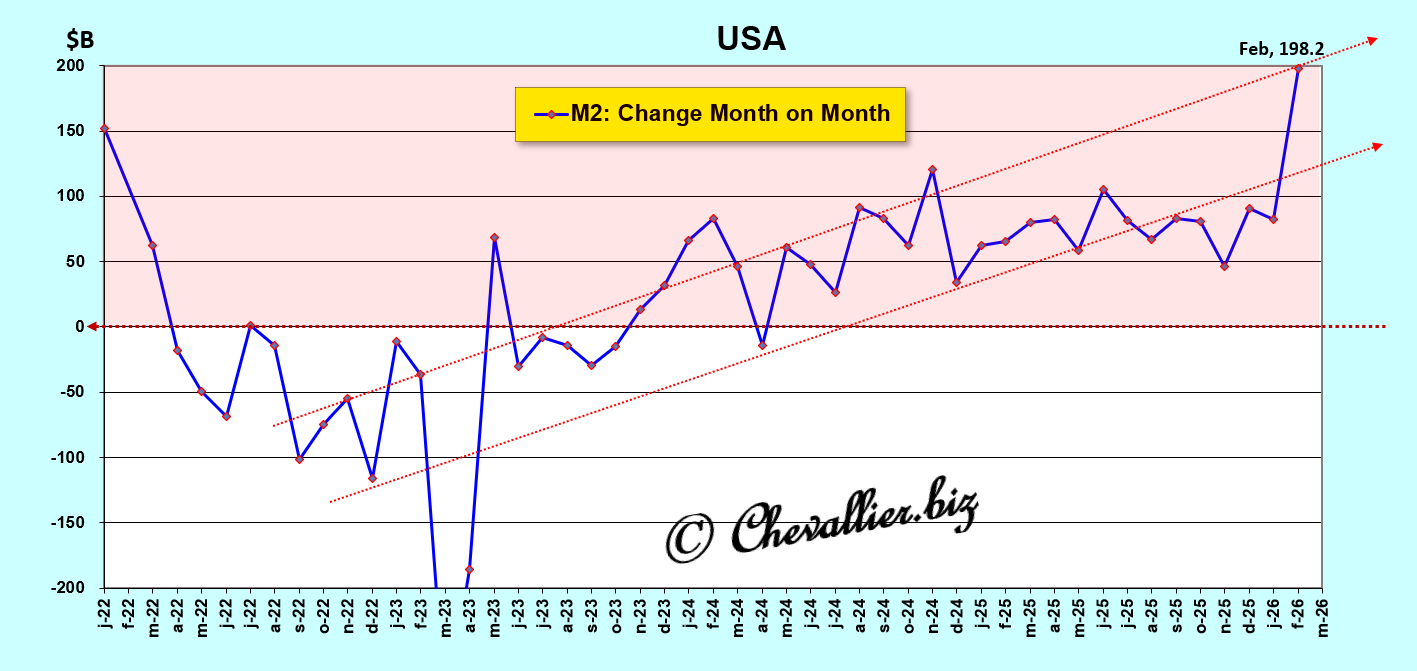

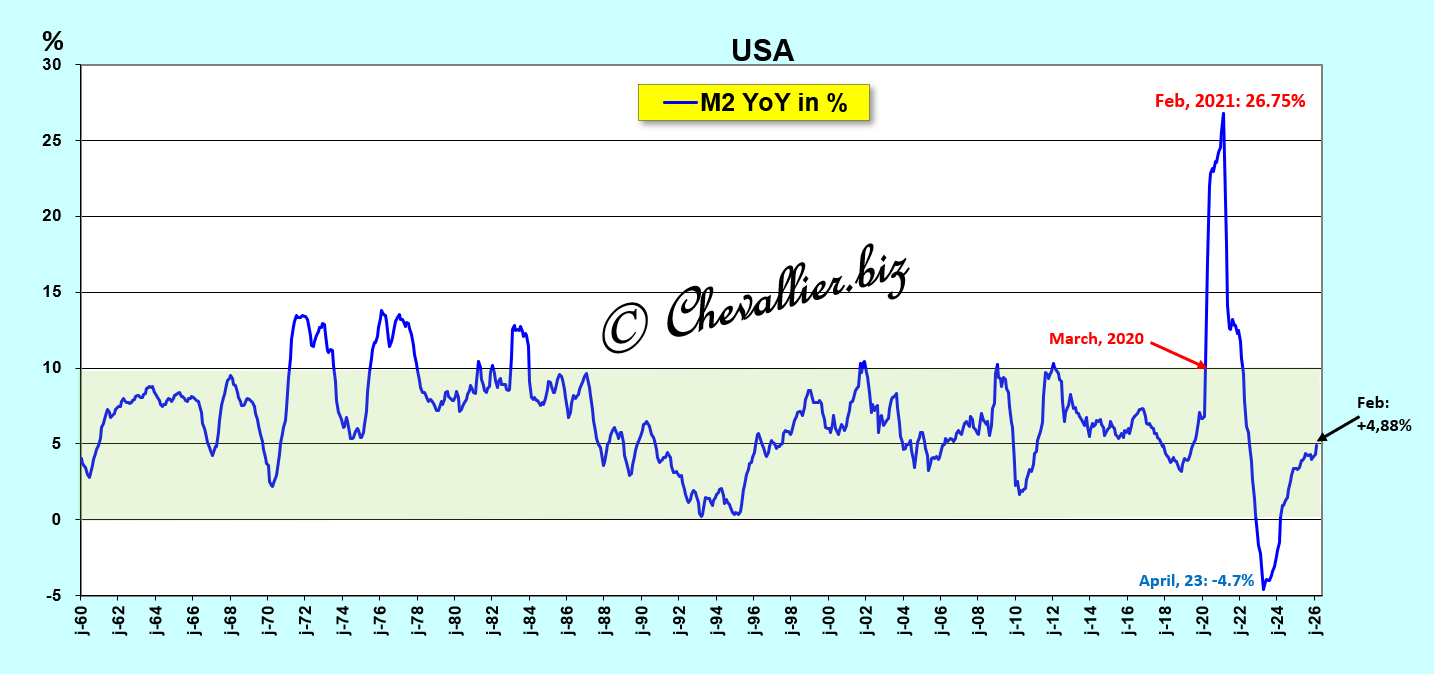

The month-over-month increase in the U.S. M2 money supply had been fluctuating within an upward trend since the end of 2022 and rebounded sharply during the month of February 2026 (latest figures published to date), reaching a peak of 198.2 billion dollars for a total of 22,667 billion dollars,

Document 1:

In other words, and more precisely, after fluctuating within a flat range in 2025, an upward trend in this M2 monetary aggregate has continued over the long period beginning in 2022, with a very sharp upward trend in February of this year.

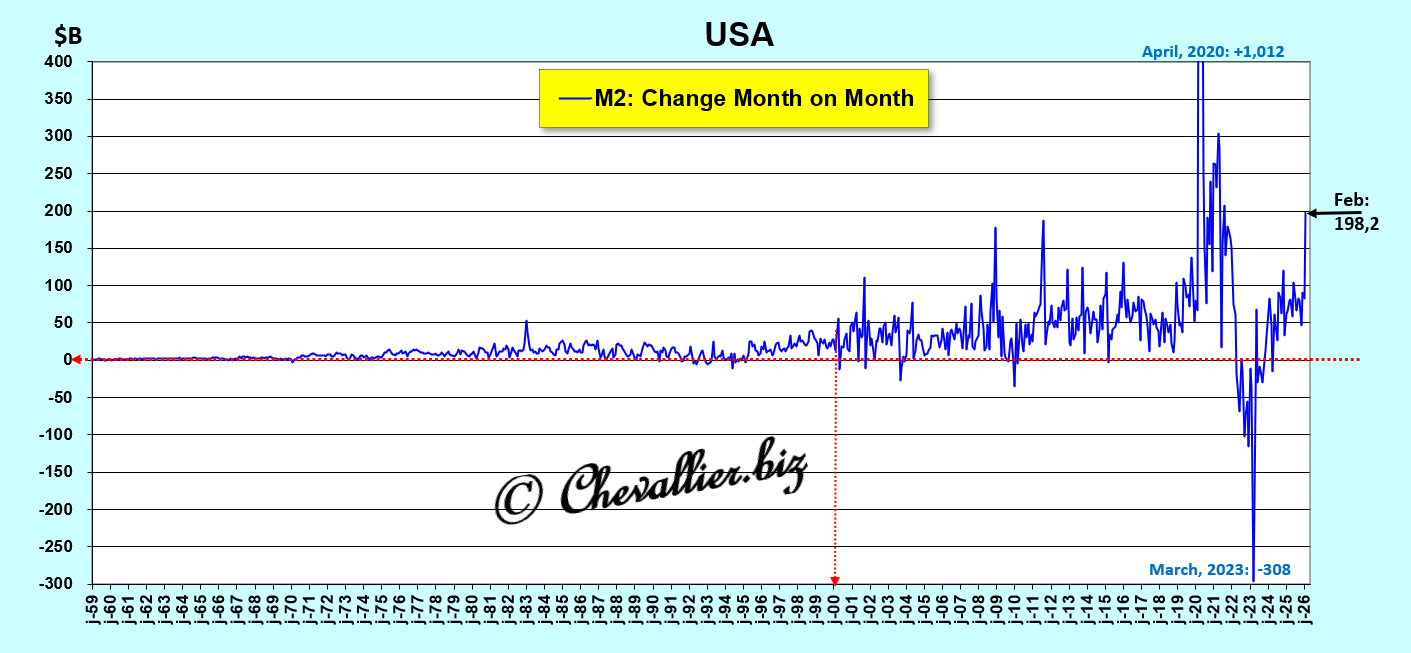

Month-over-month variations in the M2 monetary aggregate were small in the 20th century, but everything changed starting in the year 2000: these fluctuations have become massive, completely out of the ordinary, especially in 2020 (due to this coronavirus situation) and in 2023 because of the stress caused by the collapse of three U.S. banks saved from bankruptcy under extraordinary circumstances.

The increase in the M2 money supply of approximately $200 billion during February 2026, just before the outbreak of the war waged by the United States and Israel against Iran, is very significant and even extraordinary, foreshadowing severe financial turbulence.

It was possibly caused by the problems posed by private credit.

Document 2:

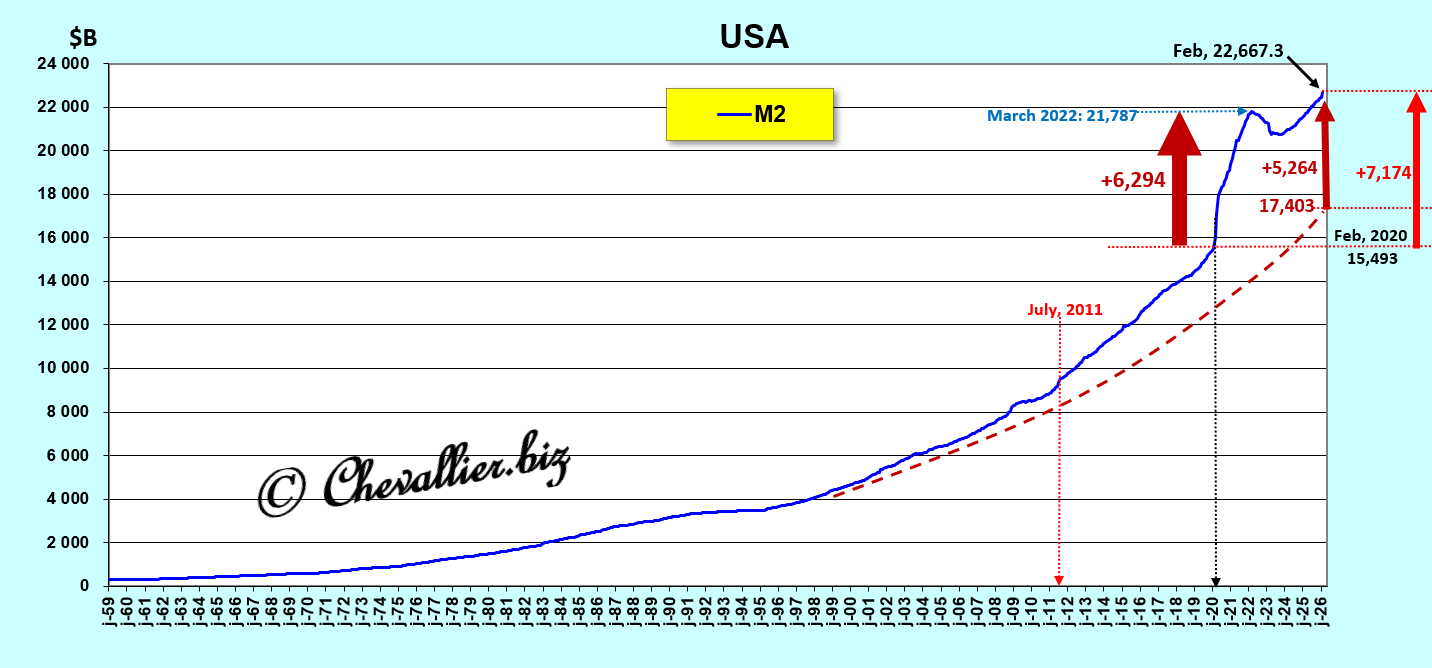

In absolute terms, the growth of this M2 monetary aggregate has once again far exceeded its long-term trend (dotted line).

At the end of February 2026, according to the latest figures published to date, this M2 monetary aggregate reached a total of $22,667.3 billion, of which… $5,264 billion was extraordinary, mainly due to $6,294 billion in undue payments resulting from this coronavirus situation,

Document 3:

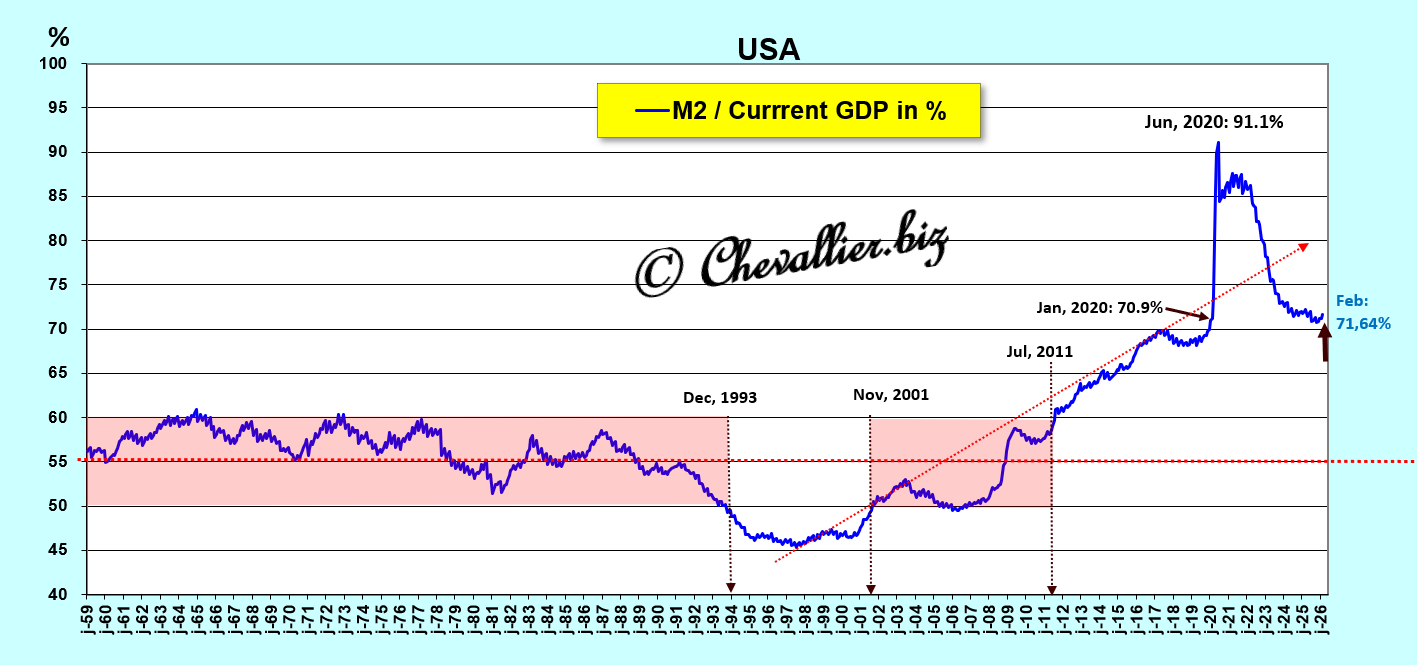

As a reminder, according to standards defined based on observations of changes in monetary aggregates since these data began being published (1959), the amount of this M2 monetary aggregate should not exceed 55% of current annual GDP.

These standards were more or less adhered to for 50 years but were exceeded after the Great Recession of 2008, skyrocketing in 2020 without returning to an acceptable range.

The increase in the M2/GDP ratio as a percentage over the month of February 2026 is small, and it is difficult to imagine it returning to normal levels in the foreseeable future,

Document 4:

This year-over-year increase in the M2/GDP ratio (as a percentage) gives the impression that it is normal, but because this ratio has exceeded the norm since 2011, the money supply remains outside the norm,

Document 5:

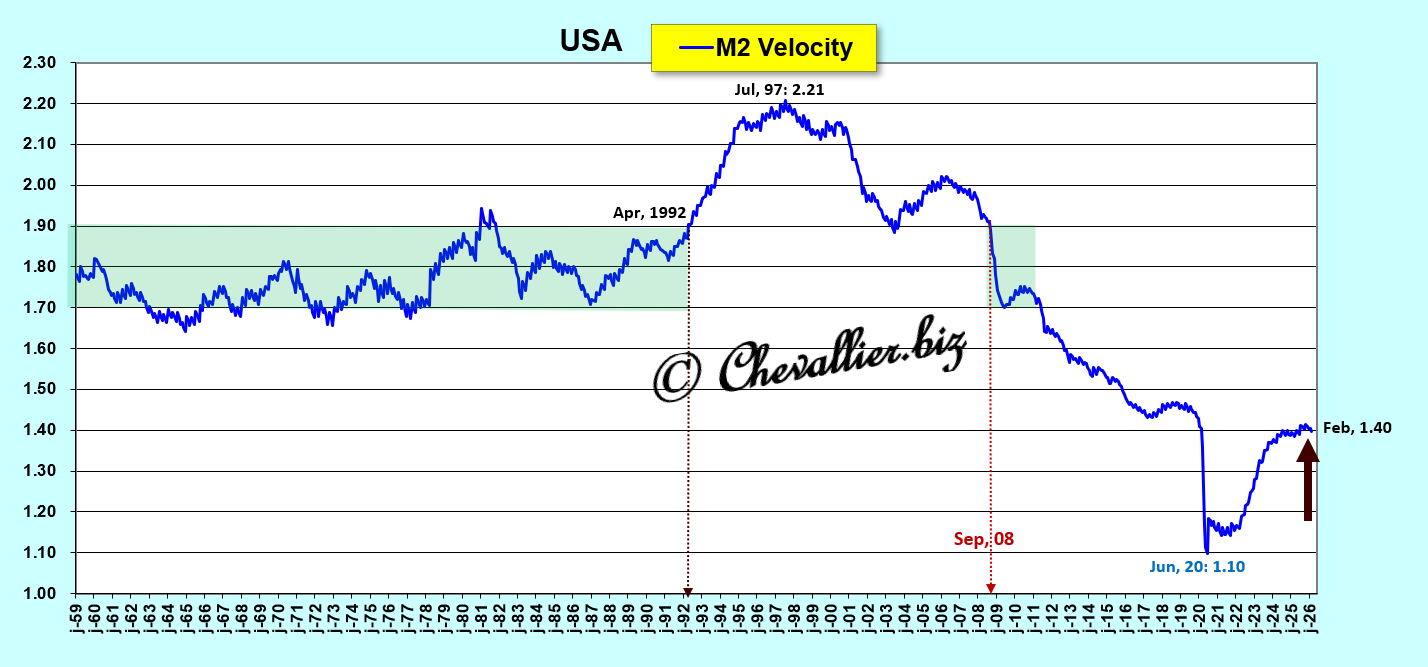

The velocity of money, which is the GDP/M2 ratio—that is, the inverse of the M2/GDP ratio (as a percentage)—calculated using the M2 monetary aggregate, fluctuated within a flat trend with a marginal decline in February.

Document 6:

***

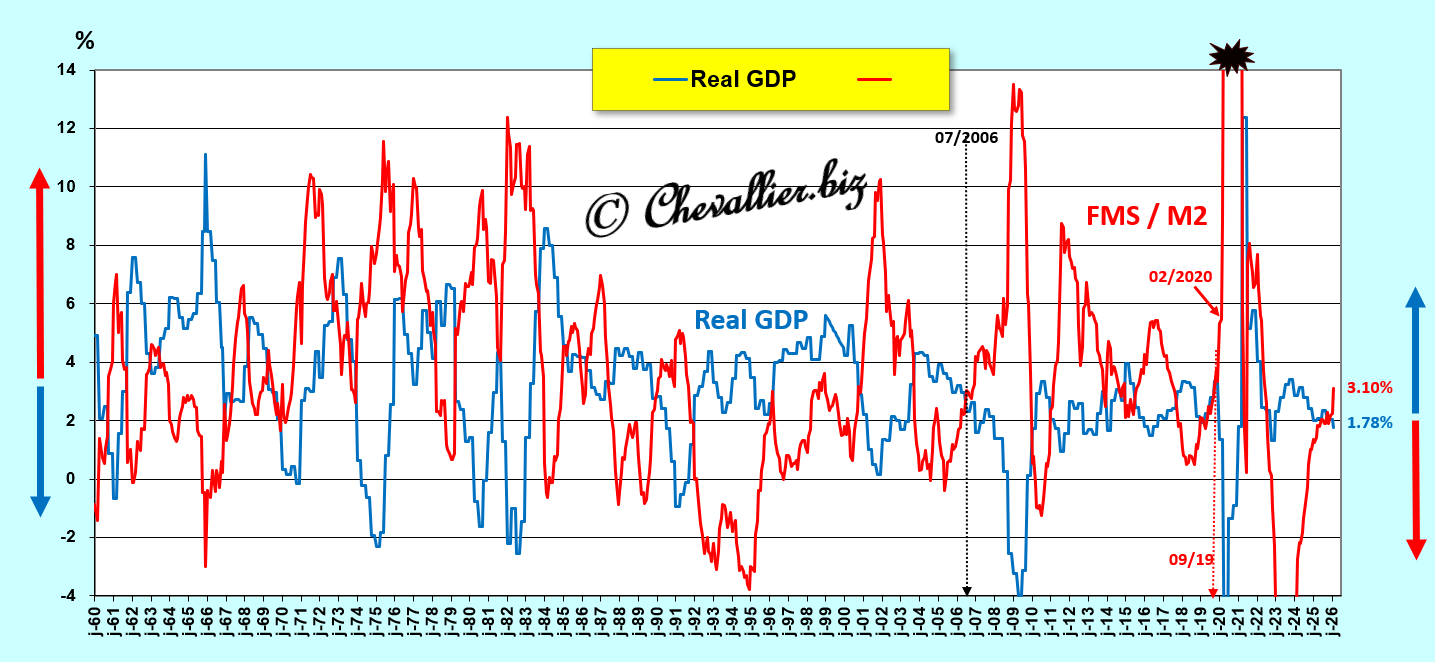

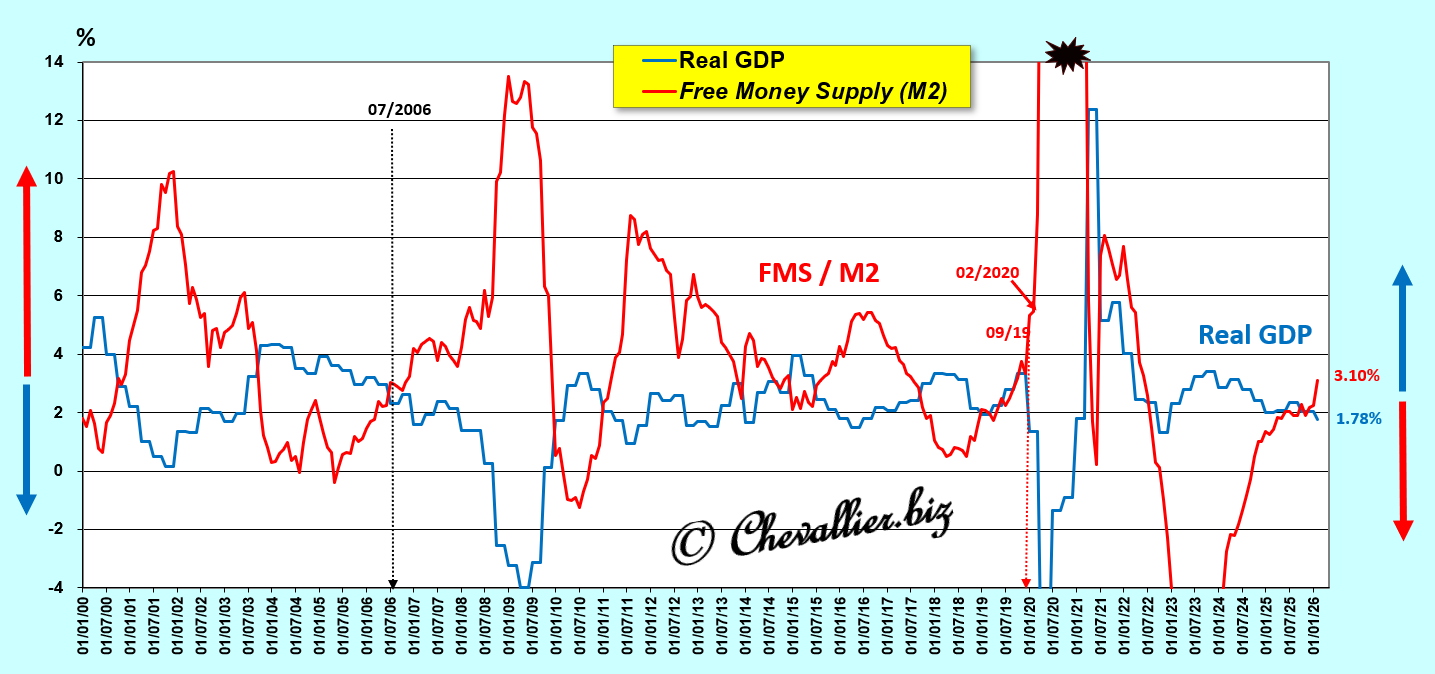

These data, thus clarified and analyzed, help us understand the relationship between changes in a nation’s money supply and those in its real GDP…

To put it simply, an increase in this M2 money supply held by Americans leads to a decline in real GDP, and vice versa, which has held true over the long term, ever since these data have been published by our friend Fred from St. Louis.

More specifically, it is the change in what I call the free money supply M2—which is the difference between, on the one hand, the change (year-over-year in percentage terms) in the M2 monetary aggregate, and on the other hand (minus) the change in real GDP (year-over-year in percentage terms)—that causes an inverse reaction in this real GDP.

The $200 billion increase in the M2 monetary aggregate in February was thus already enough to contribute to a significant decline in real GDP for the first quarter of 2026!

Document 7:

A closer look at the recent period since the early 2000s shows more precisely this decline in GDP, which is not negative based on changes in the M2 monetary aggregate as of February but will be very sharp in the second quarter due to the war against Iran and the monetary bubble.

Document 8:

The increase in the M2 monetary aggregate should logically continue in the coming months, particularly due to the inflation caused by this war against Iran, which will exacerbate the decline in GDP in the United States and everywhere else in the world due to shortages of certain hydrocarbon-related products and disruptions in supply chains.

***

Analyses and conclusions regarding the impact of changes in monetary aggregates on real GDP have not been taken into account by financial market participants for the past twenty years, even though these are the very issues and solutions that underpin the economic activity of any nation.

This is why Ben Bernanke took care to ensure that the Fed would no longer publish weekly figures for the M1, M2, and M3 monetary aggregates from the moment he took office as Fed chairman in February 2006.

Subsequently, Jerome Powell added another layer of opacity by publishing only monthly data for the M2 monetary aggregate.

Thus, only those acting internally have access to this fundamental data and can manipulate financial communications and financial markets at will!

This increase in the M2 monetary aggregate can be explained by the fact that Americans had already anticipated in February a possible worsening of their financial situation and thus generally increased their precautionary savings (M1-M2).

These Americans are the consumers and savers who form the foundation of economic activity, and they are also voters who may express their dissatisfaction in the upcoming midterm elections.

***

Click here to read my previous article on this topic.

Click here to view this article on my website in French.

© Chevallier.biz