The significant increase in the U.S. M3 money supply in March did not cause a decline in real GDP, in accordance with my law of the free money supply, because the monetary bubble is extraordinary.

***

We live in an increasingly financialized world, yet paradoxically, economists are attaching less and less importance to what is fundamentally crucial: the relationship between the money supply and wealth creation, that is, GDP.

Yet this was the major issue that the monetary authorities of so-called Western countries monitored very closely and successfully during the second half of the 20th century.

The purpose of this article is to return to these fundamentals and bring them up to date…

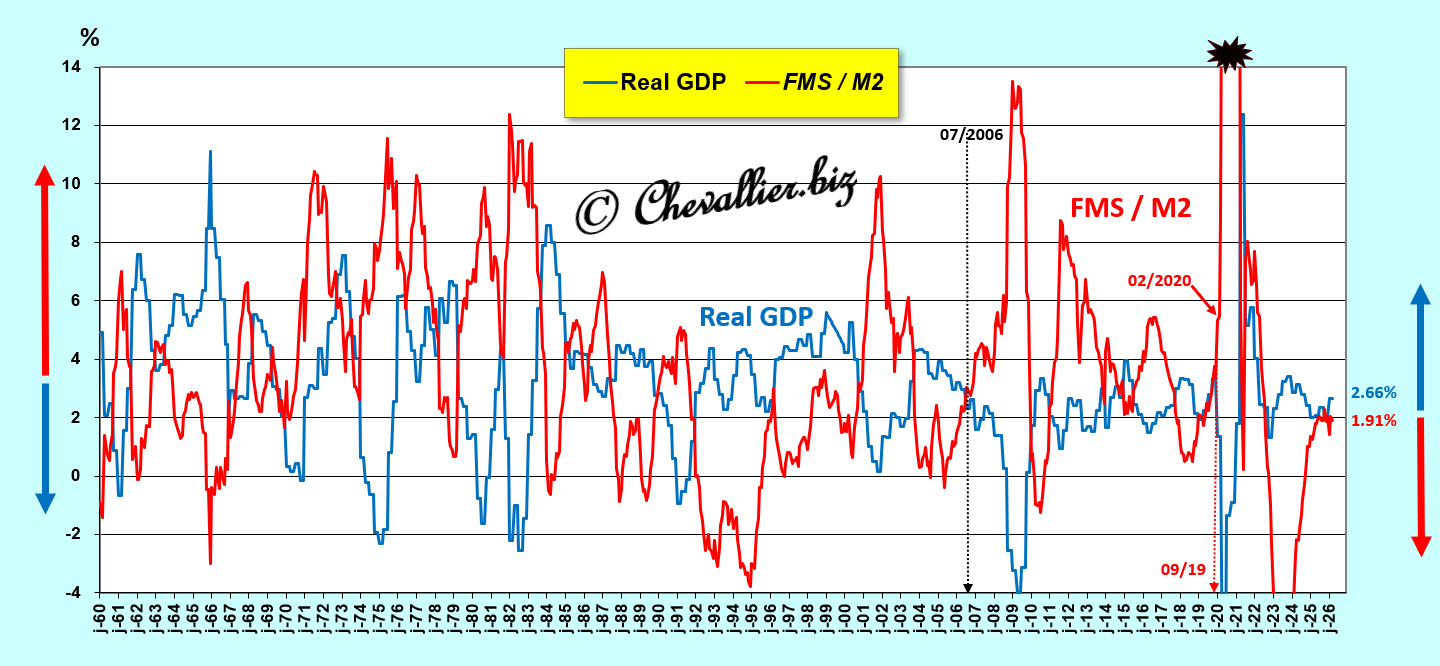

Essentially, and to simplify, an increase in the M3 money supply held by Americans leads to a decline in real GDP, and vice versa.

Arthur Laffer’s maxim, “sound money is the first pillar of Reaganomics”, is now nothing more than a distant memory of a bygone era…

***

Every fully independent and sovereign country has its own currency.

However, the example of Germany between the two world wars showed that when a nation’s monetary authorities allow monetary expansion to spiral out of control, a major economic crisis ensues, and it can even have catastrophic consequences on a global scale.

This is why, after World War II, the monetary authorities of developed countries acted vigorously and effectively to prevent the formation of a monetary bubble in Western nations, a task that Karl Otto Pöhl accomplished remarkably well while he presided over the Bundesbank.

Thus, during the second half of the 20th century, all central bank governors in the so-called free world perfectly controlled fluctuations in monetary aggregates to keep them within optimal limits, without, however, defining them theoretically or empirically in relation to a baseline entity, namely GDP.

However, it is possible to define these limits (by quantifying them) based on the statistical series published by the Fed over the long term, since the postwar period, which helps us better understand that it is the fluctuations in monetary aggregates that are the primary and fundamental cause of fluctuations in real GDP (in the opposite direction), all else being equal.

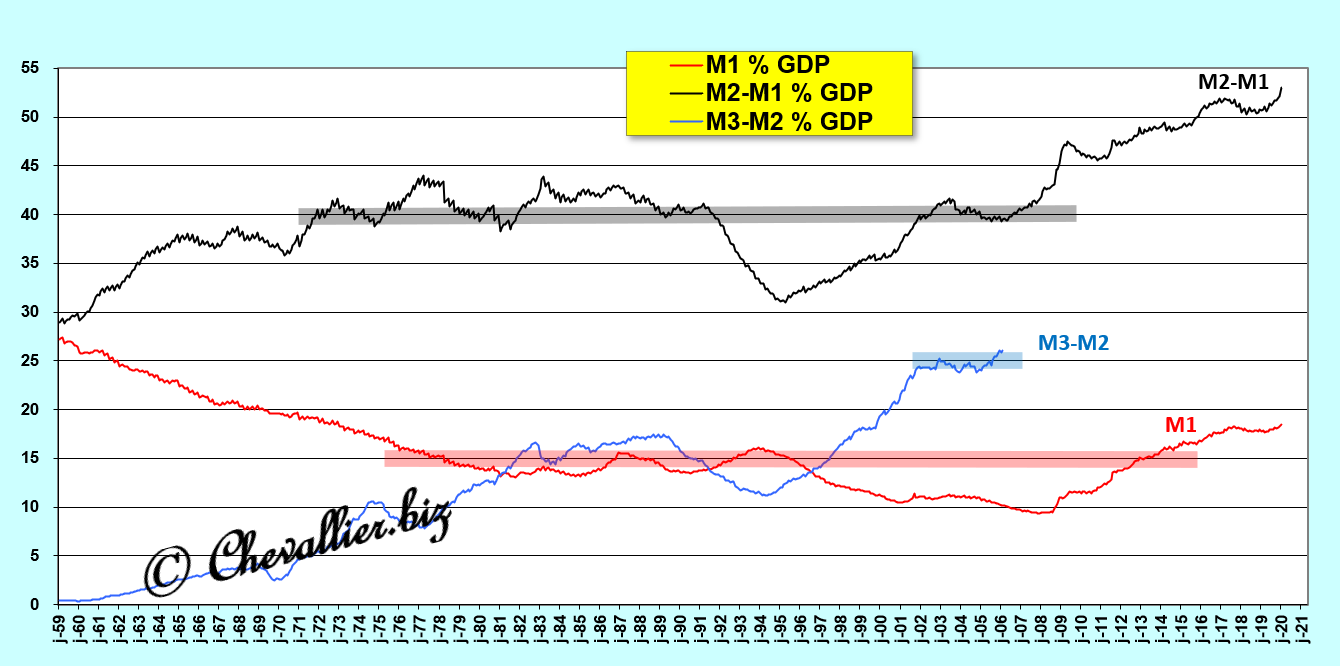

As a reminder, a nation’s total money supply, denoted M3, is the sum of three monetary aggregates…

The monetary aggregate M1 is the sum of positive current account balances and currency in circulation, and the M1/GDP ratio (as a percentage) must not exceed 15% of annual current GDP.

The monetary aggregate M2 consists of the sum of the M1 aggregate and the M2-M1 aggregate, which includes savings account deposits. This M2-M1/GDP ratio (as a percentage) must be less than 40% of current GDP.

Finally, the M3-M2 aggregate corresponds to the total cash holdings of corporations and money market funds. This M3-M2/GDP ratio (as a percentage) must be less than 25% of current GDP.

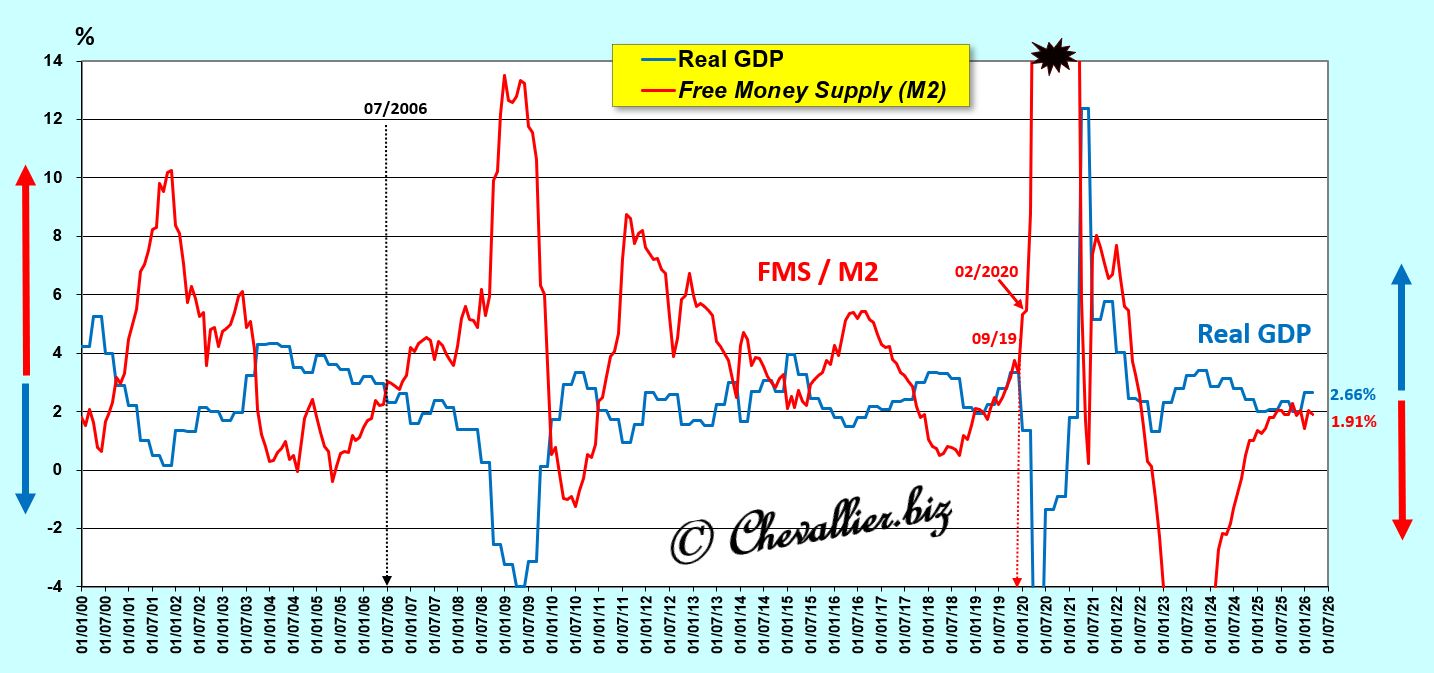

These limits were never exceeded simultaneously in the United States prior to 2006,

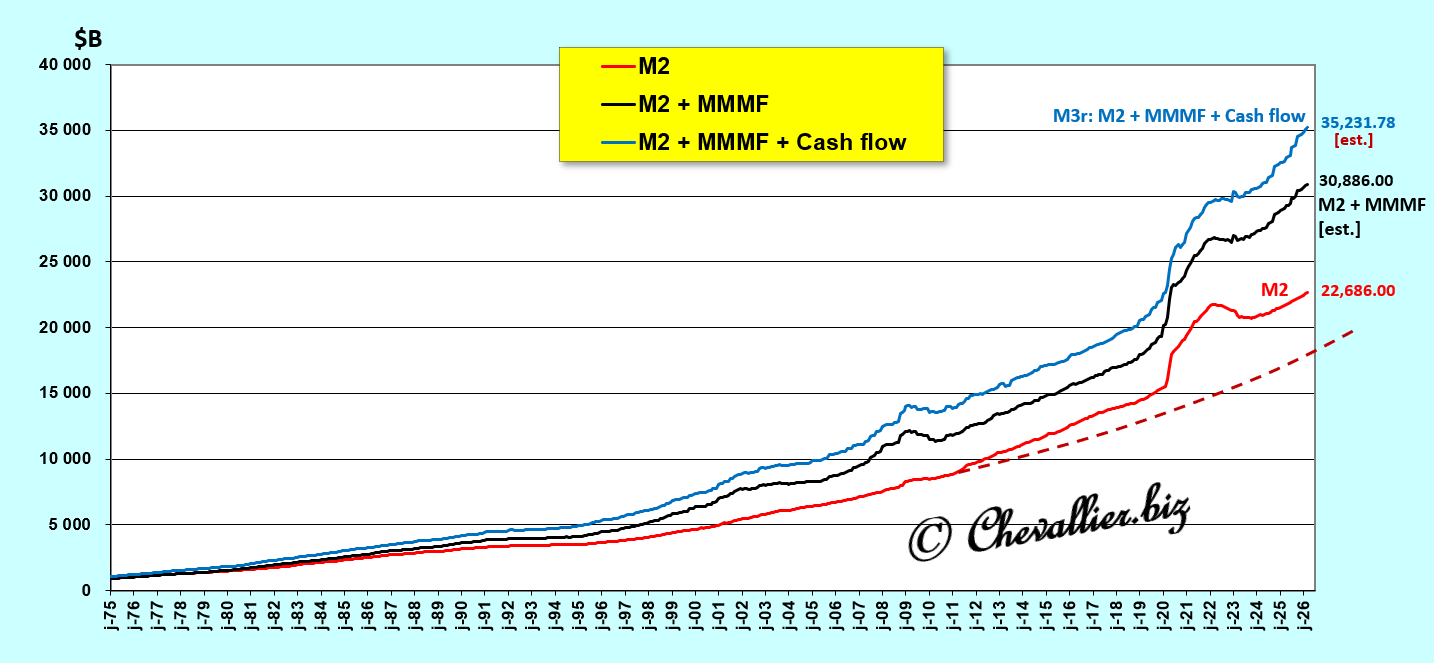

Document 1:

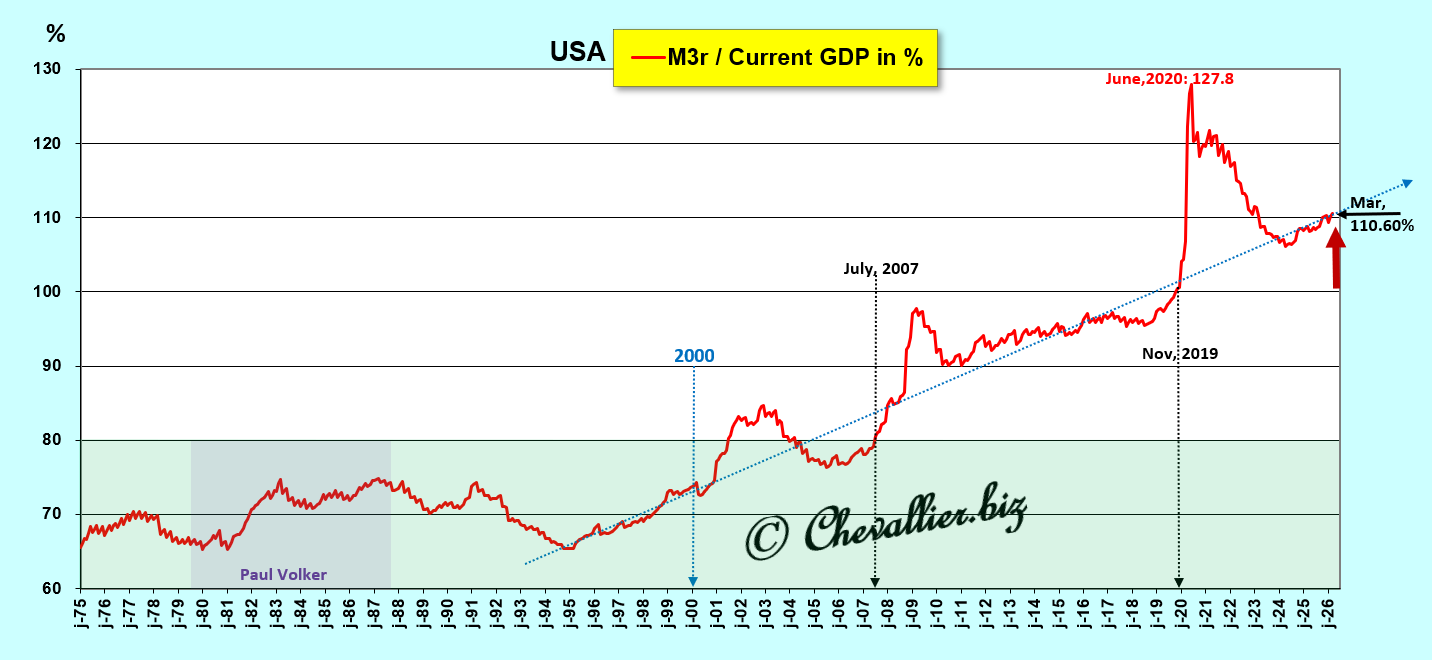

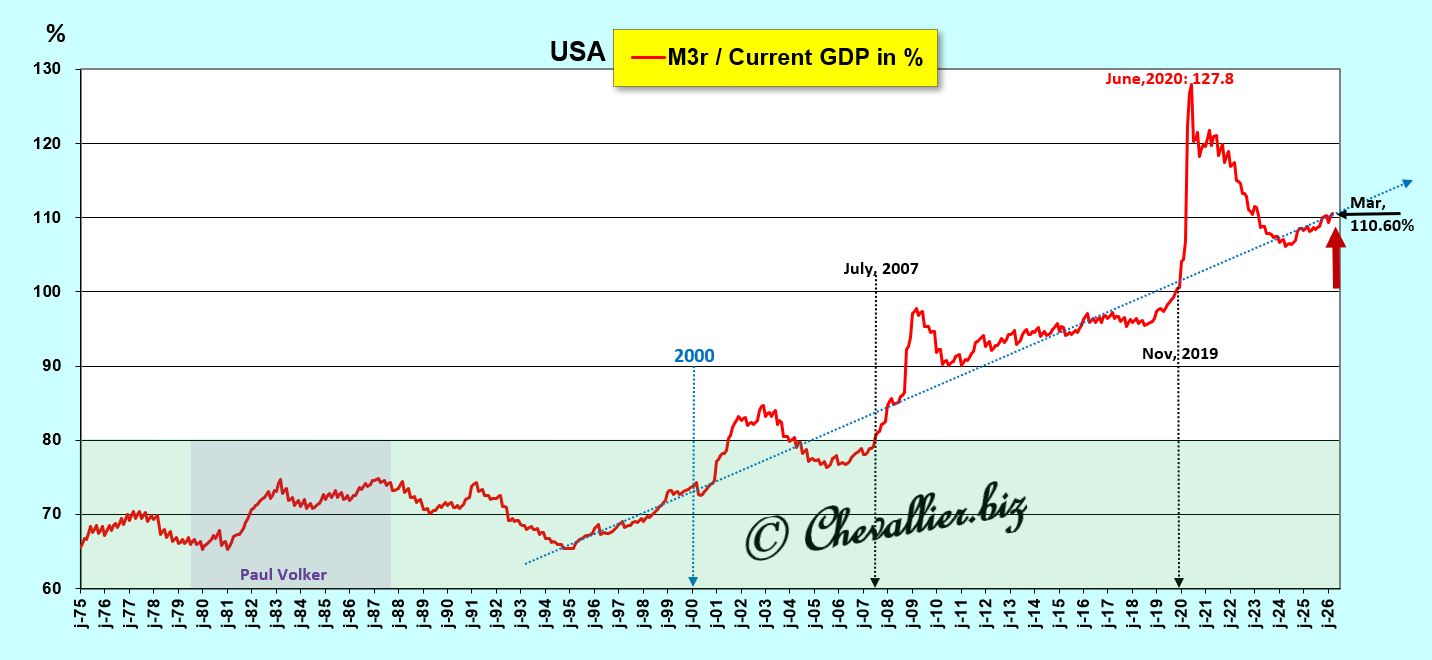

Thus, the M3/GDP ratio (as a percentage) should never exceed 80% of current GDP.

This raises a problem: Ben Bernanke had the publication of the total U.S. money supply, M3, banned as soon as he took office as Fed Chair in February 2006 so that monetarist economists could no longer analyze it and draw conclusions that are nonetheless essential!

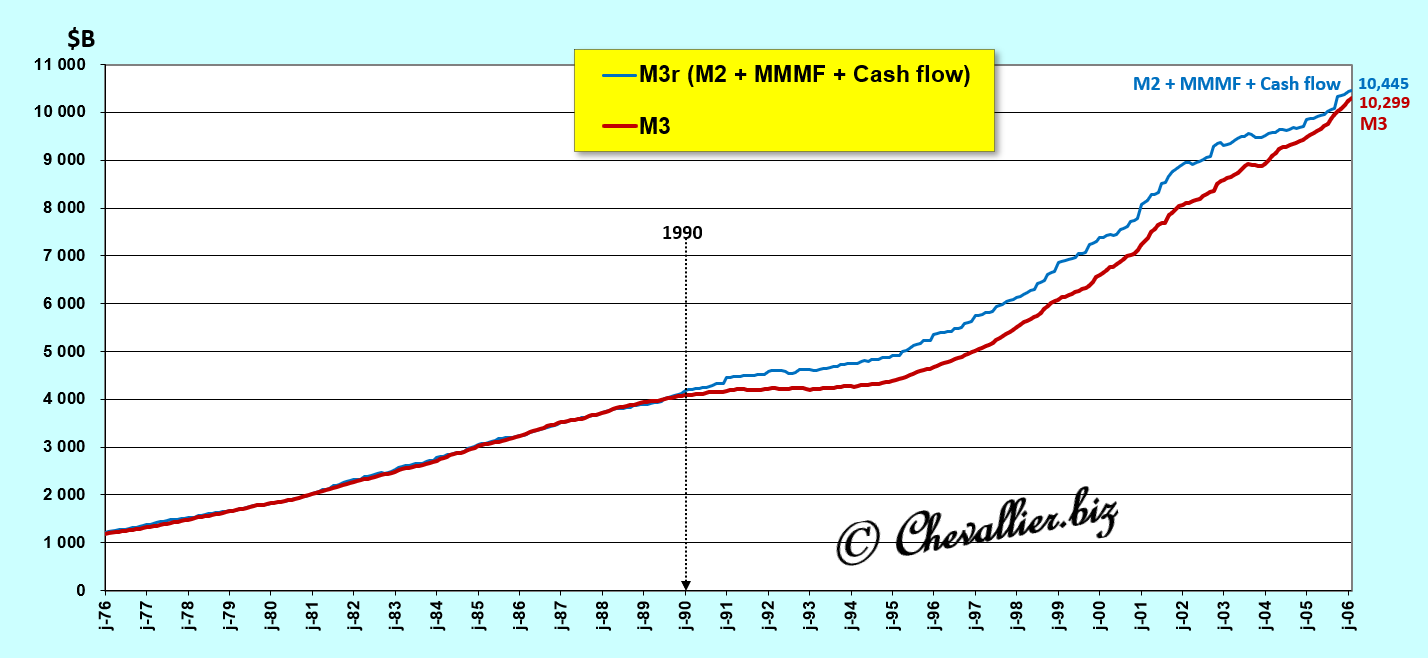

However, I have managed to reconstruct the amount of the U.S. M3 money supply, which I denote as M3r with an r for revised, based on the components that make up the M3-M2 aggregate, which are still published elsewhere…

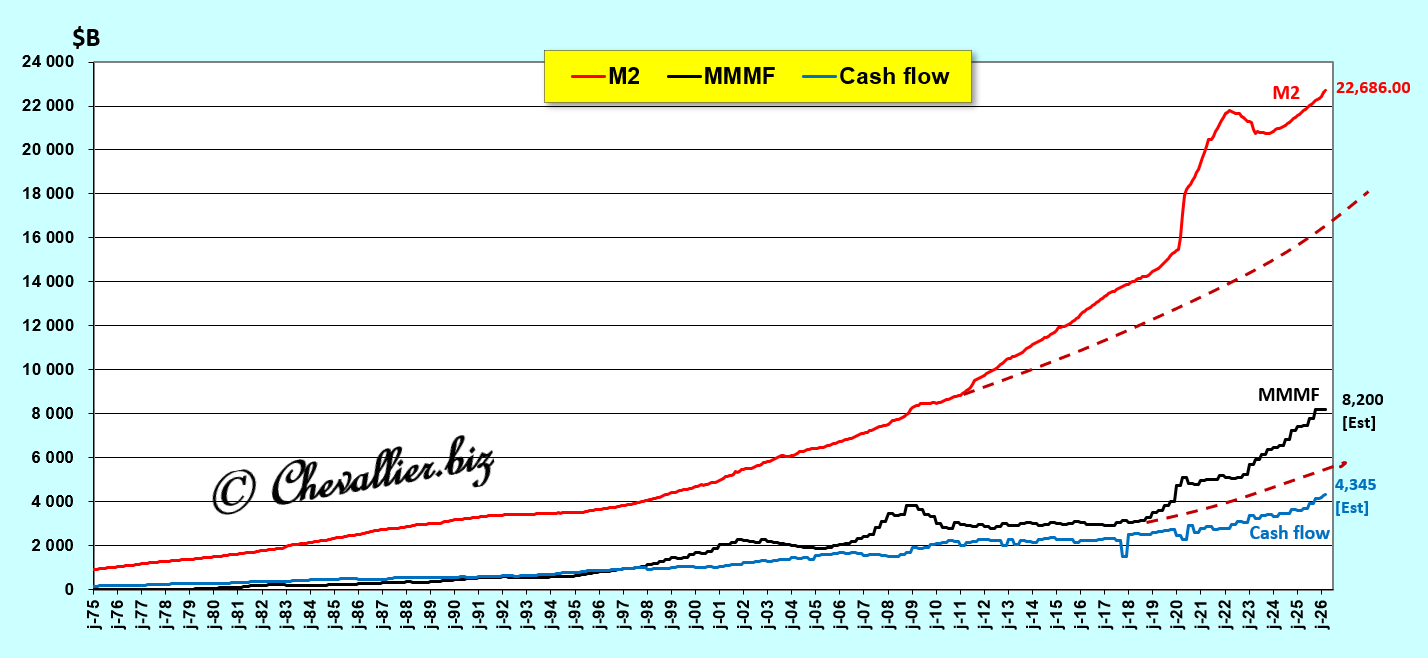

Indeed, a nation’s total money supply M3 consists, on the one hand, of the monetary aggregate M2 (whose figures are still published monthly in the United States) and, on the other hand, of money market mutual funds (MMMF) and corporate net cash flow.

Our friend Fred from St. Louis publishes this data quarterly for Money Market Mutual Funds (MMMF) under the code MMMFFAQ027S and for corporate net cash flow under the code CNCF.

Thus, for the period from 1976 to 1990, the curves derived from the series published by our friend Fred de Saint Louis based on M3 aggregate figures (published by the Fed) coincide perfectly with those of the M3r figures calculated from the M2 aggregate, money market mutual funds, and corporate net cash flow.

Subsequently, a divergence becomes apparent, which eventually tends to resolve itself in 2006.

Document 2:

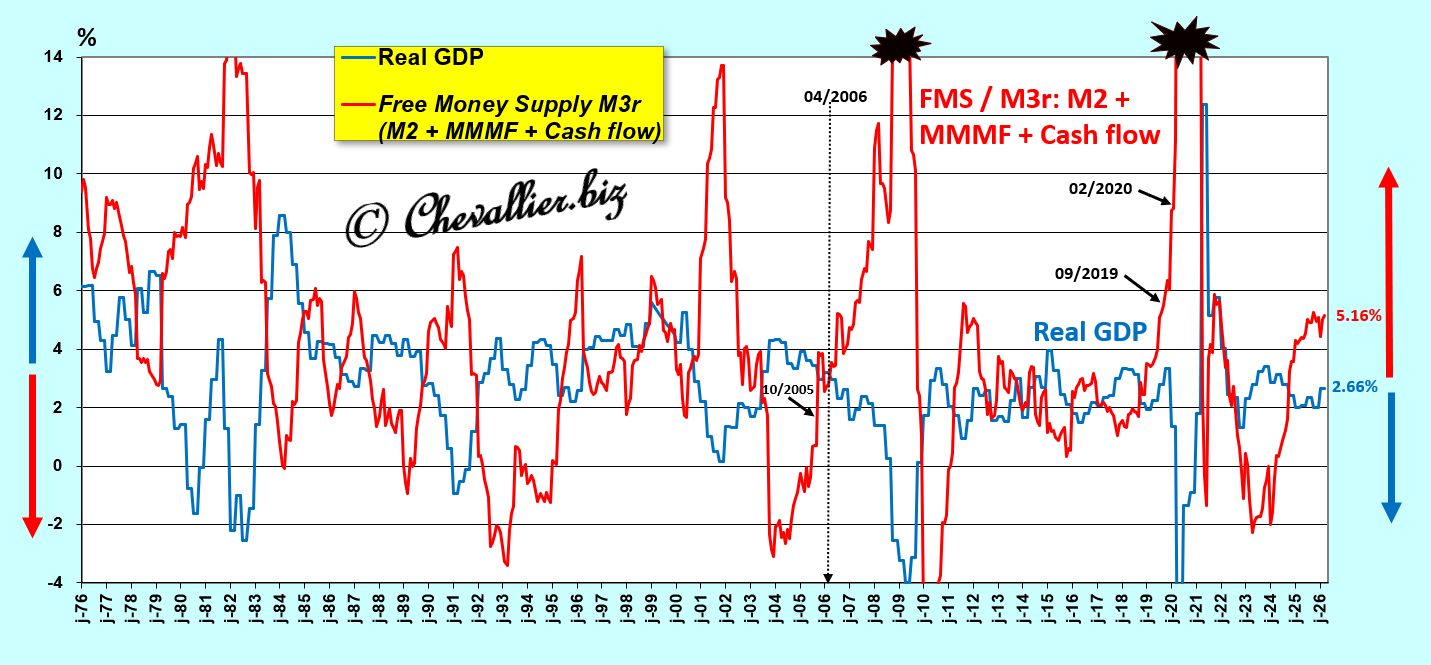

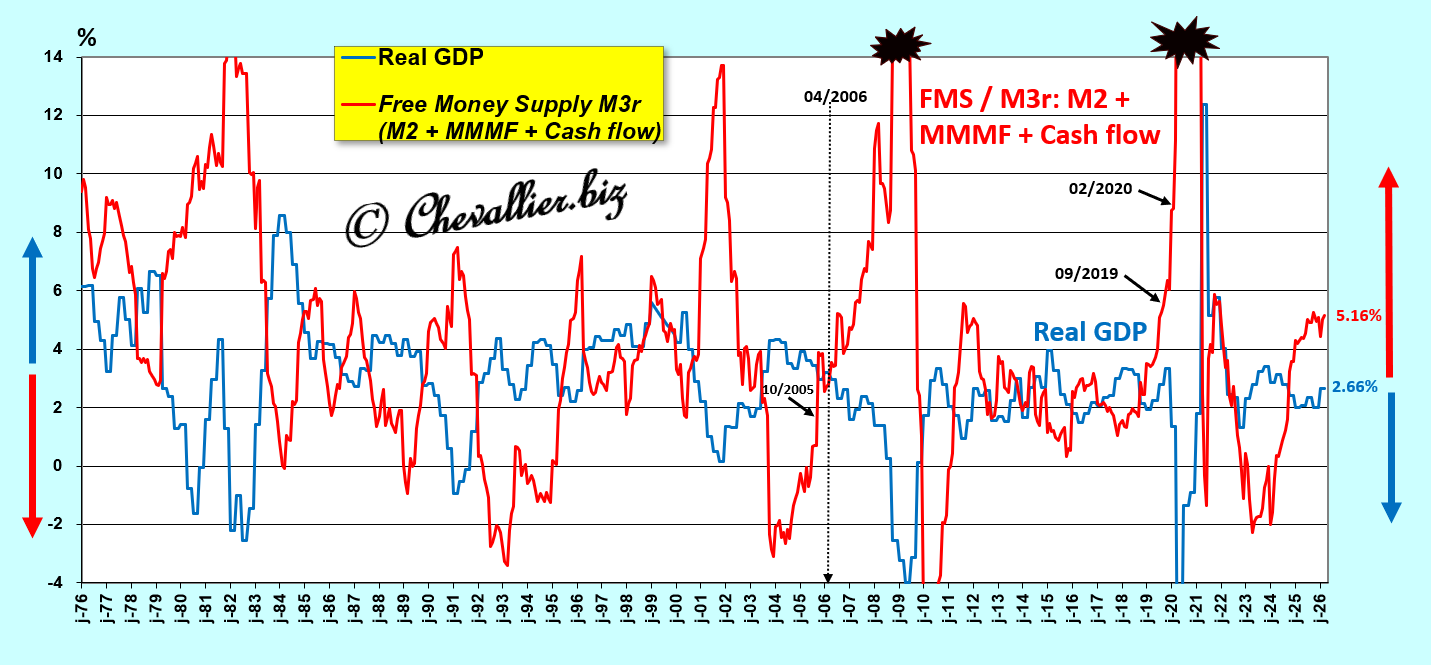

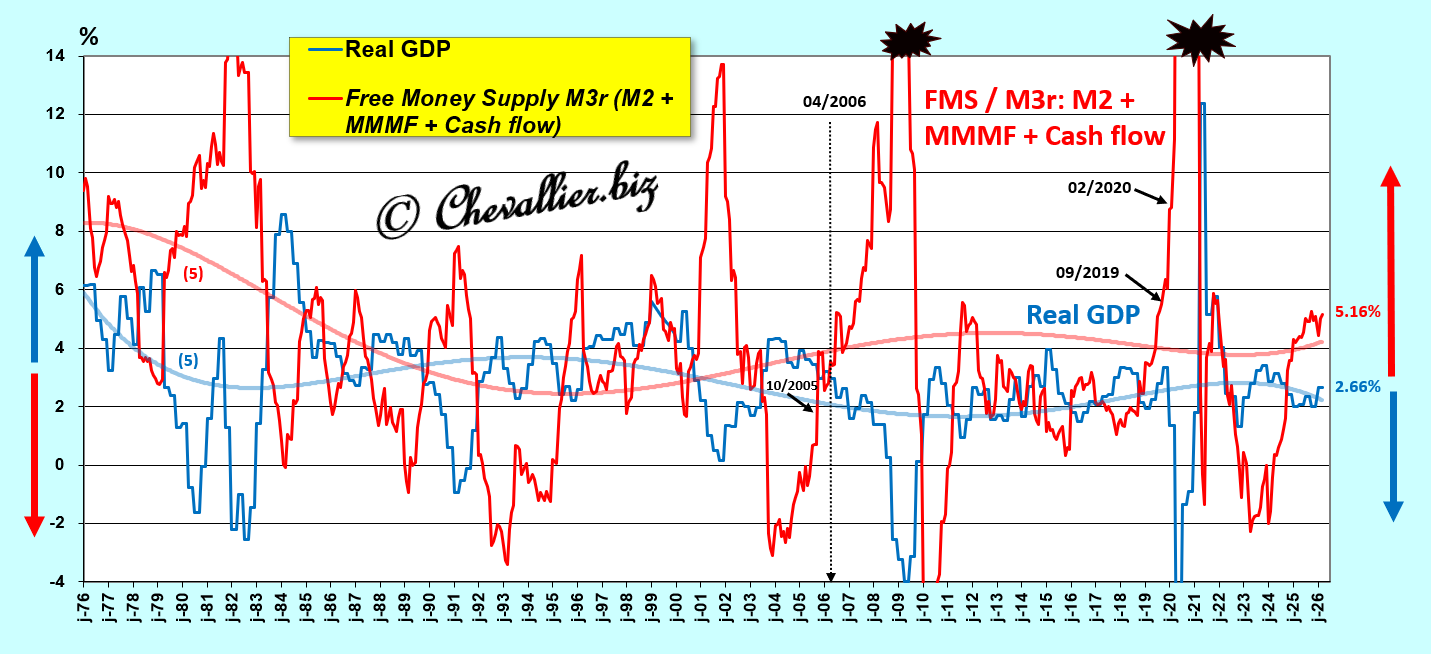

Consequently, based on the redefinition of the U.S. M3 money supply from 1976 to the present, it is possible to apply this law of free money supply using monthly data on the M3r money supply, whose fluctuations inversely determine those of real GDP.

It then appears (to simplify) that an increase in the M3 money supply held by Americans leads to a decline in real GDP, and vice versa, which holds true over the long term, since 1976 when these data have been published by our friend Fred from St. Louis.

More precisely, it is the change in what I call the free money supply, M3, which is the difference between, on the one hand, the change (year-over-year in percentage terms) in the M3 money supply, and on the other hand (minus) the change in real GDP (year-over-year in percentage terms), that causes a reaction inversely proportional to the change in that real GDP.

Document 3:

We will therefore analyze, in the first part, the characteristics of the changes in the M3r money supply, and then, in the second part, the changes in real GDP relative to those of the free money supply M3r.

***

Part One: Analysis of the Characteristics of Changes in the M3r Monetary Aggregate

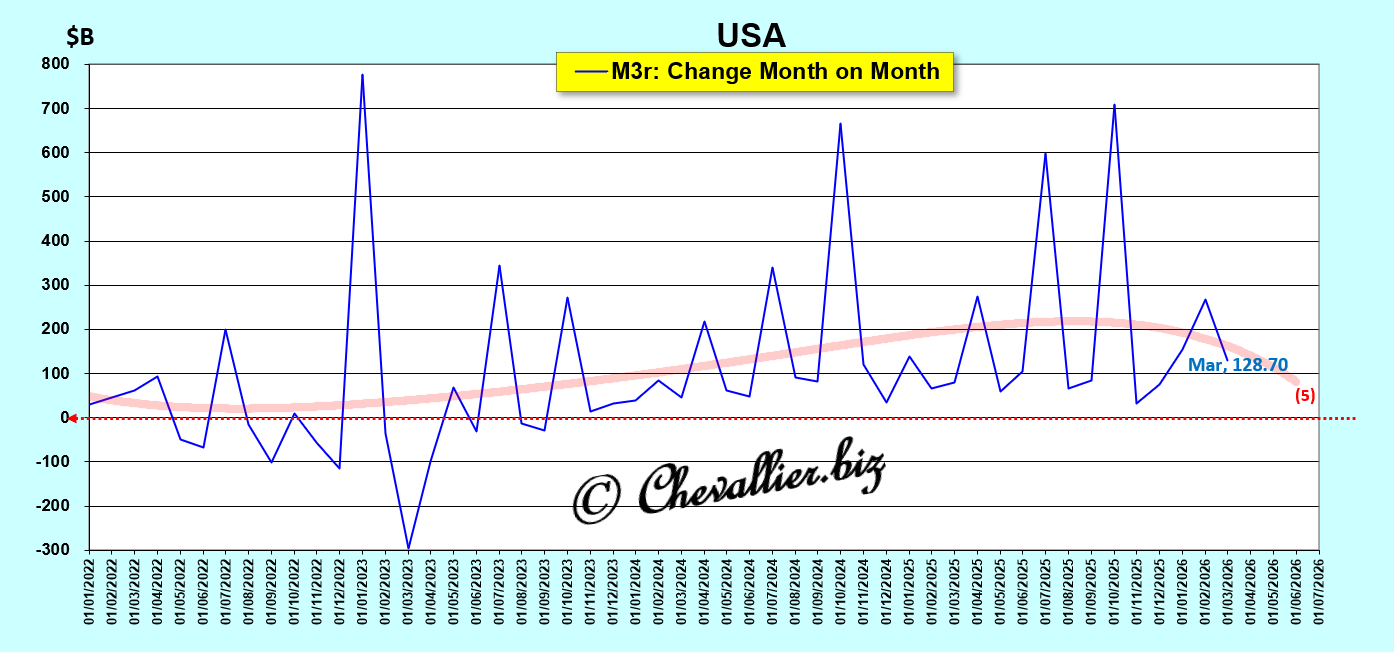

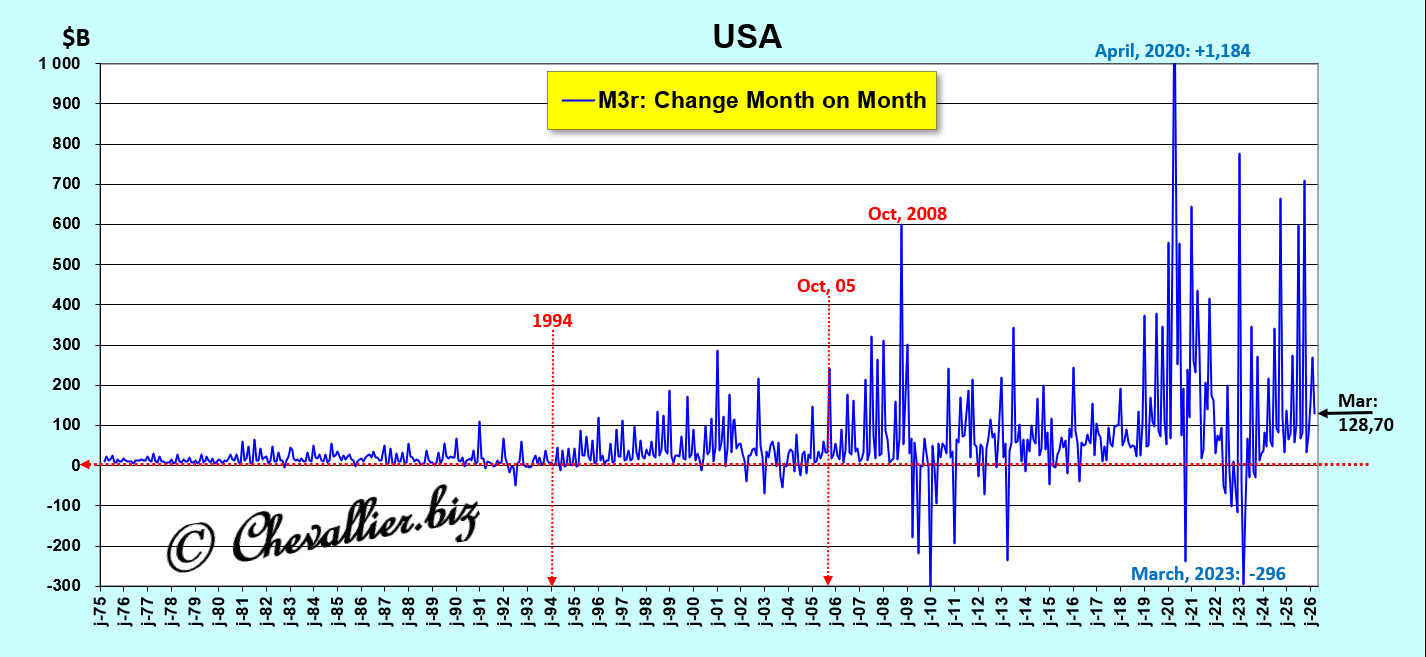

During the first quarter of 2026 (the latest figures published to date), the month-over-month increase in the U.S. M3r money supply continued to fluctuate at the lower end of a range of $100 to $200 billion since the beginning of 2022, though occasionally with sharp, short-lived rebounds,

Document 4:

Month-over-month fluctuations in the M3r money supply were small in the 20th century, but everything began to change starting in 1994, with these fluctuations intensifying before the Great Recession of 2008 (beginning in October 2005), and becoming completely out of the ordinary in the final months leading up to 2020 and this coronavirus situation,

Document 5:

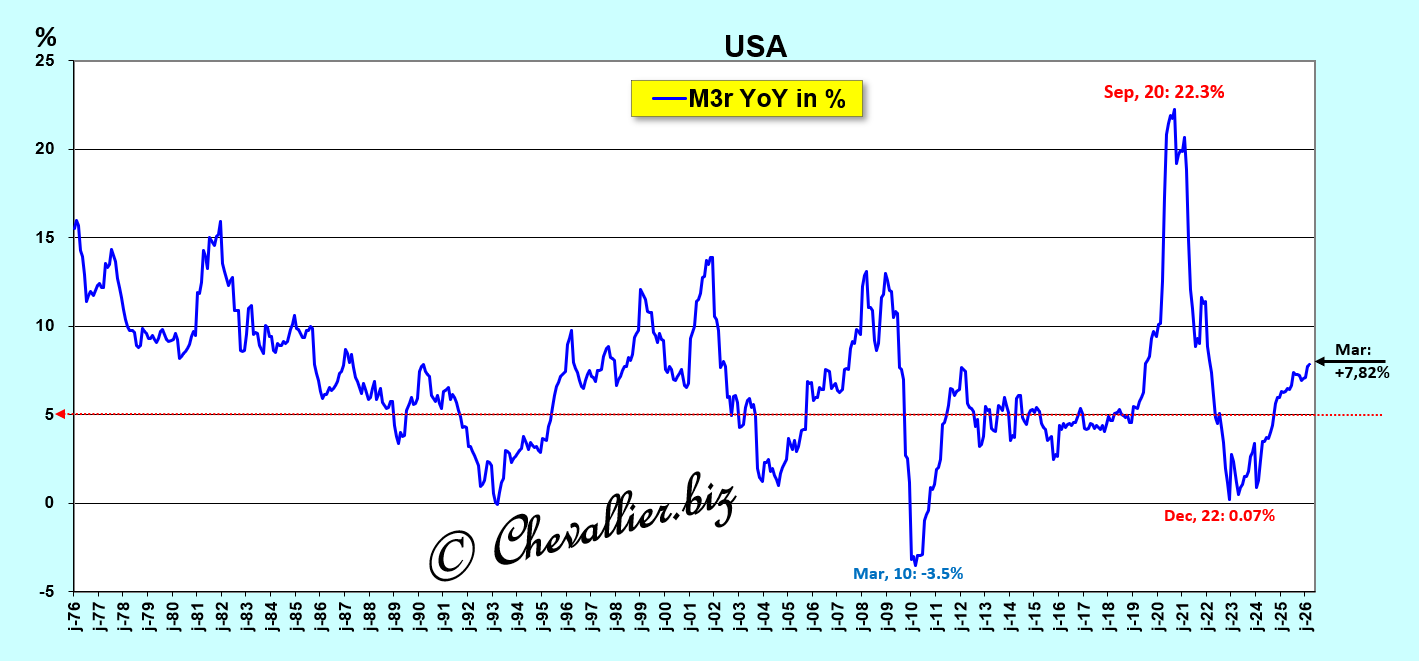

The year-over-year increase in this money supply M3r was 7.8% in March (the latest figures published to date), which is higher than the historical trend of around 5% and the current GDP growth rate for the first quarter of 2026, which was 6.0%,

Document 6:

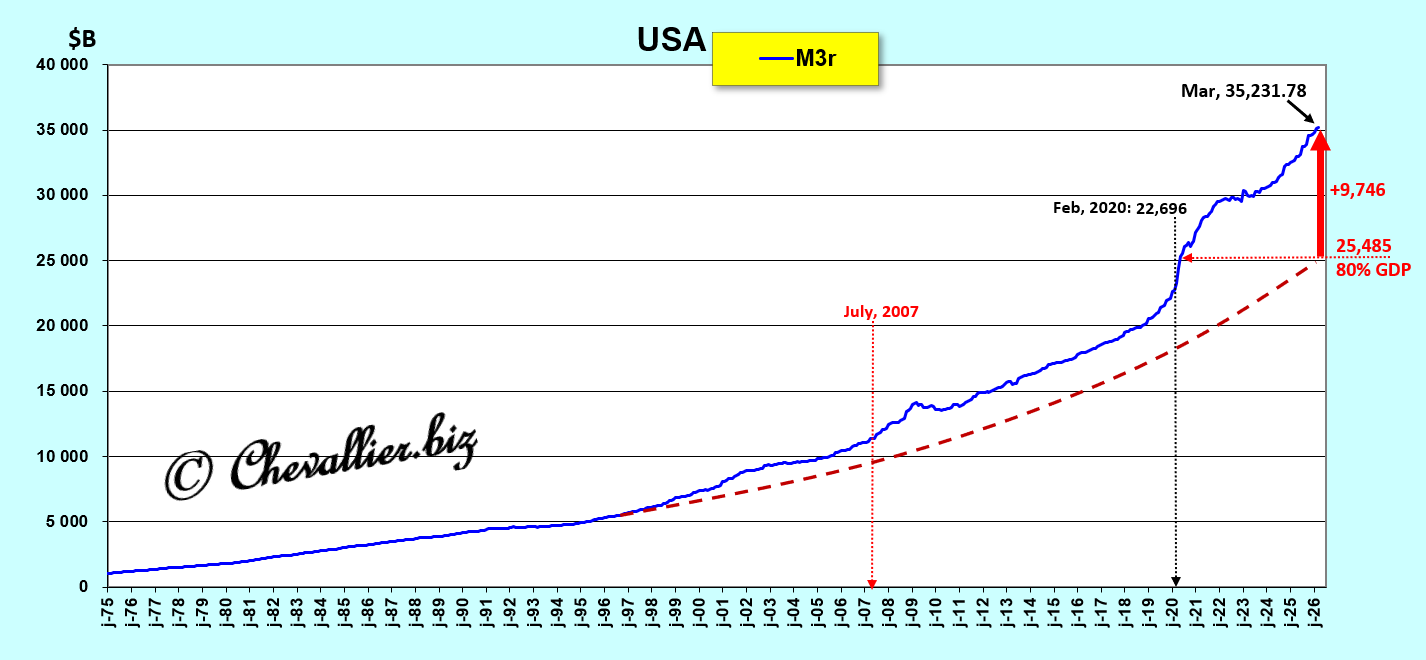

At the end of March 2026, this M3r money supply reached a total of $35,231.78 billion, of which…$9,746 billion was above normal (i.e., exceeding the 80% of GDP threshold), especially since this coronavirus situation.

In absolute terms, the growth of this M3r money supply has once again far exceeded its long-term trend, which should have been normal (dotted line), i.e., remaining below 80% of current GDP,

Document 7:

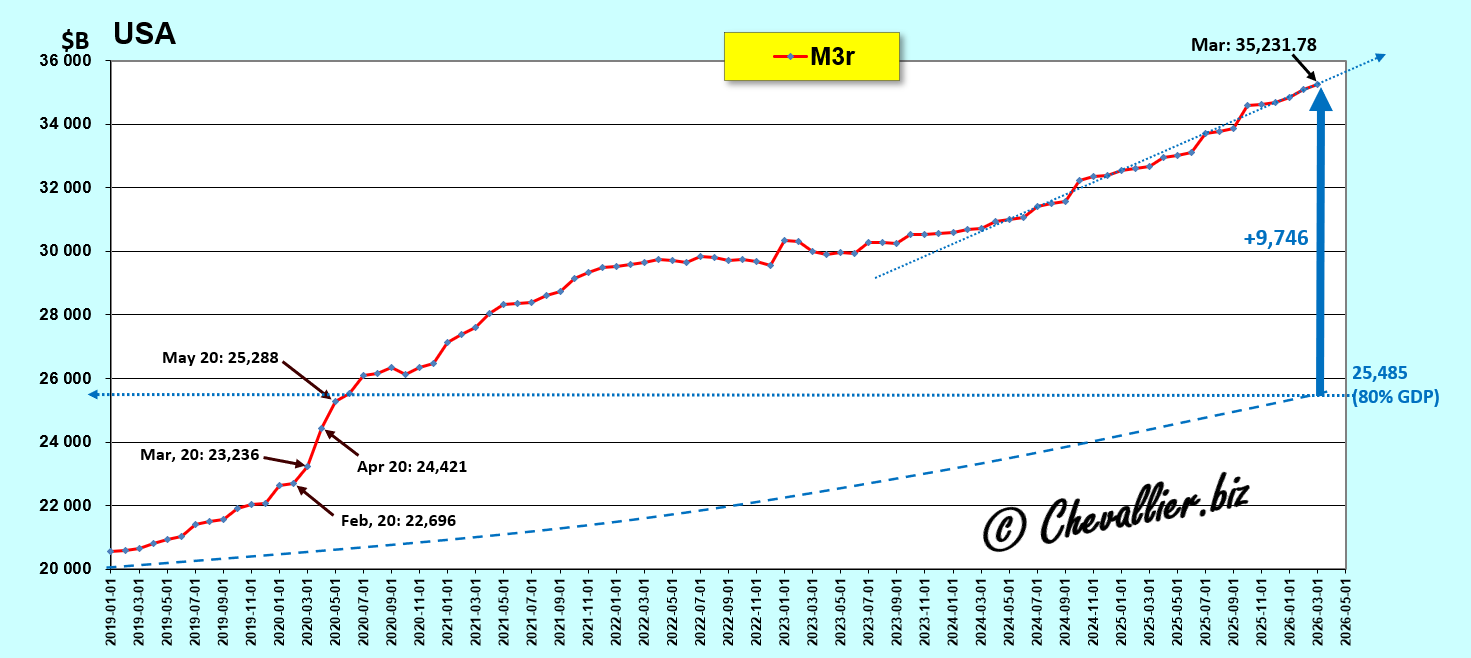

A closer look at the recent period shows that this M3r money supply continues to far exceed its 2020 peak in connection with this coronavirus situation,

Document 8:

As a reminder, according to standards defined based on observations of changes in monetary aggregates since these data have been published (1959), the amount of this M3r money supply should not exceed 80% of current annual GDP.

These standards were more or less adhered to for 50 years but were exceeded following the Great Recession of 2008, skyrocketing in 2020 without returning to an acceptable range, continuing to fluctuate around 110% of current GDP,

Document 9:

It is this excessive growth of the M3 money supply that has, since 2007, created these fundamental economic imbalances, which have had and will have lethal consequences in the long term in the United States and elsewhere in the world.

During the second half of the 20th century, FOMC members consistently succeeded in keeping M3 within an optimal fluctuation band (below 80% of GDP) by raising the Fed’s base rate whenever there was a risk of exceeding the limits. Since 2008, such measures have failed to produce the expected positive effects, precisely because of this monetary expansion.

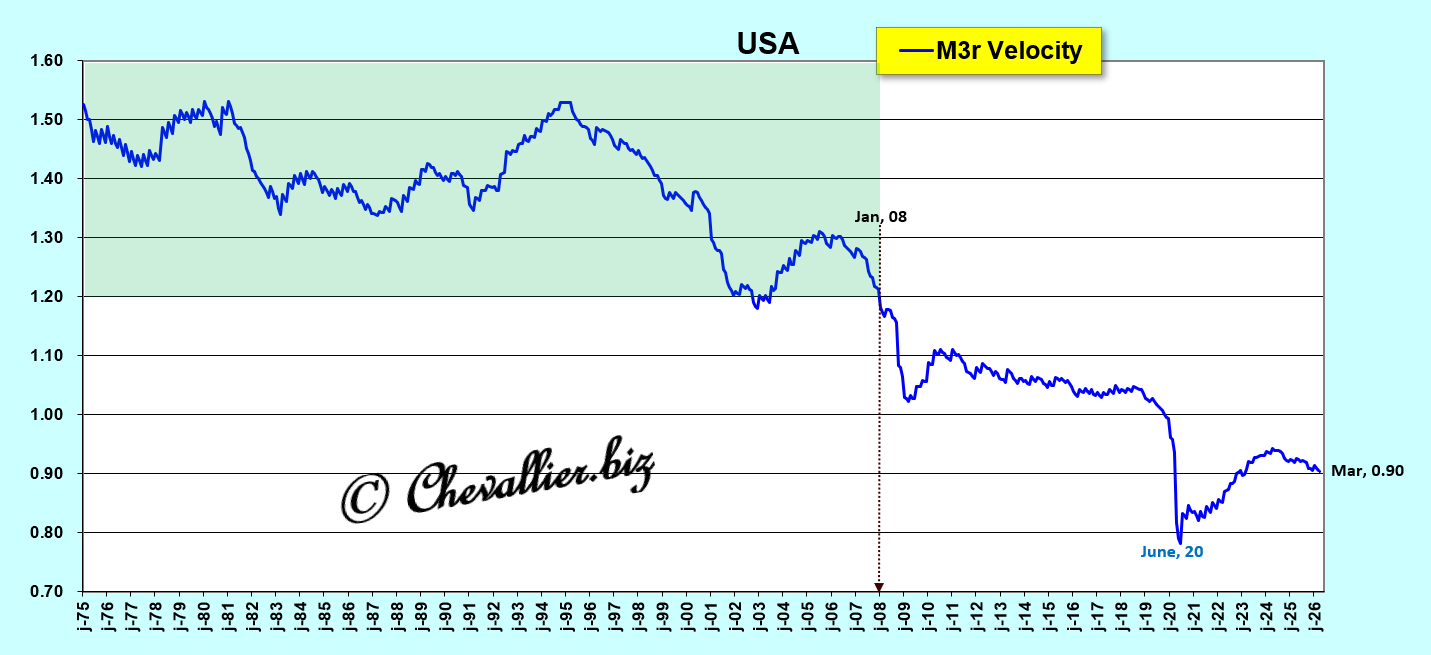

Furthermore, it is possible to analyze these monetary issues differently based on the velocity of money which is the GDP/M3 ratio, that is, the inverse of the M3/GDP ratio in percentage terms analyzed previously.

This velocity of circulation of the money supply is a concept useful for educational purposes because it helps explain that the faster money circulates, the more growth is stimulated, and vice versa.

Thus, for example, during periods of strong GDP growth, consumers do not hesitate to spend their income quickly and to invest. The velocity of circulation of money is then high, that is, well above 1.

Conversely, when a crisis is anticipated, consumers tend to set money aside (by increasing their precautionary savings) to cope with a foreseeable, uncertain future that generates fear. The velocity of money is then low, that is, less than 1,

Document 10:

Thus, to continue reliably analyzing the consequences of changes in the M3 money supply in the United States after 2006, the M3-M2 monetary aggregate must be redefined using data on money market funds and total corporate cash holdings.

These data are published quarterly later than GDP figures, and the latest figures currently available are those for the fourth quarter of 2025.

It is therefore essential at this time to estimate them correctly in order to have reliable figures for total money supply over the long period beginning in 1976.

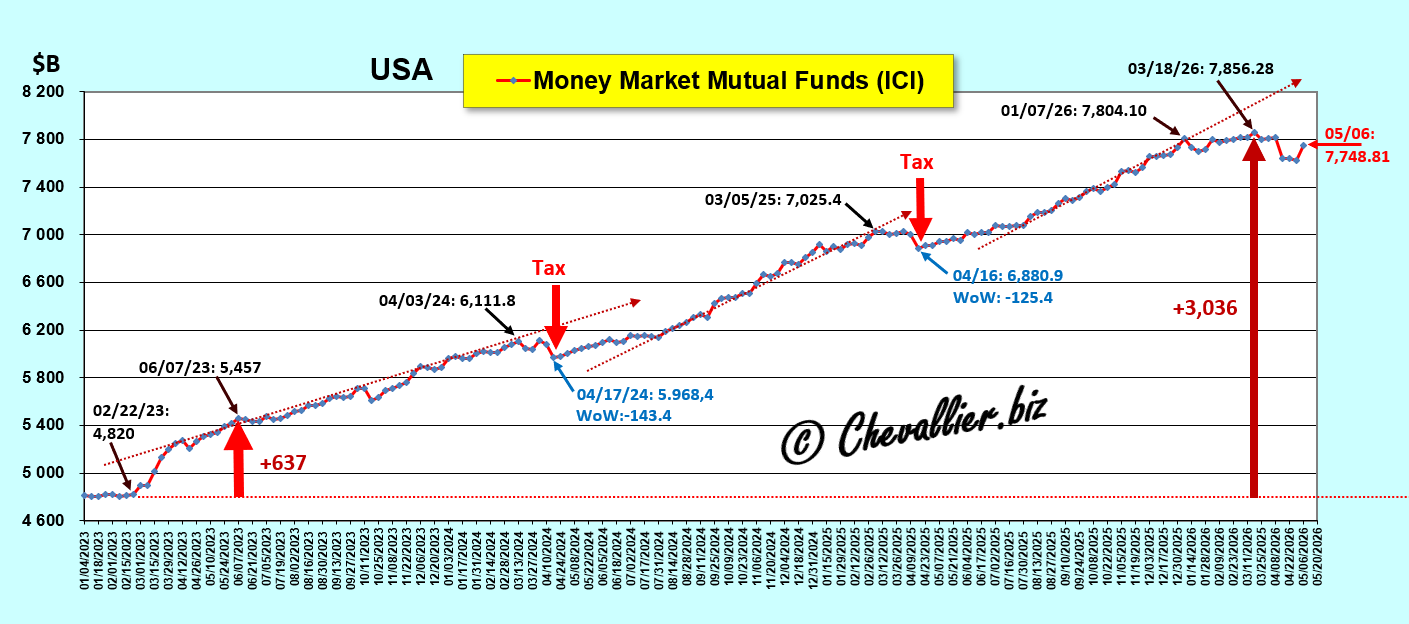

Thus, money market fund figures for the first quarter of 2026 are logically estimated to be stable compared to those of the previous quarter, consistent with the stability of the figures published by the ICI (Investment Company Institute), which are released weekly but on slightly different bases than those of our friend Fred from St. Louis; click here to access these ICI-published data,

Document 11:

The change in corporate cash holdings is estimated to be identical to that of the two previous quarters, thereby providing the most accurate picture possible of the reality of the components of the M3r money supply.

These curves, drawn from statistical series published by U.S. authorities, highlight that the increase in this hypertrophy of the M3r money supply was primarily driven from 2020 to 2022 by the extraordinary rise in the M2 monetary aggregate and by that of money market funds (except in the first quarter of 2026) and, to a lesser extent, by the rise in corporate cash flows,

Document 12:

The dashed lines correspond to what would have been the normal trend of the series.

Document 13:

***

Part Two: The Law on Free Money Supply M3r

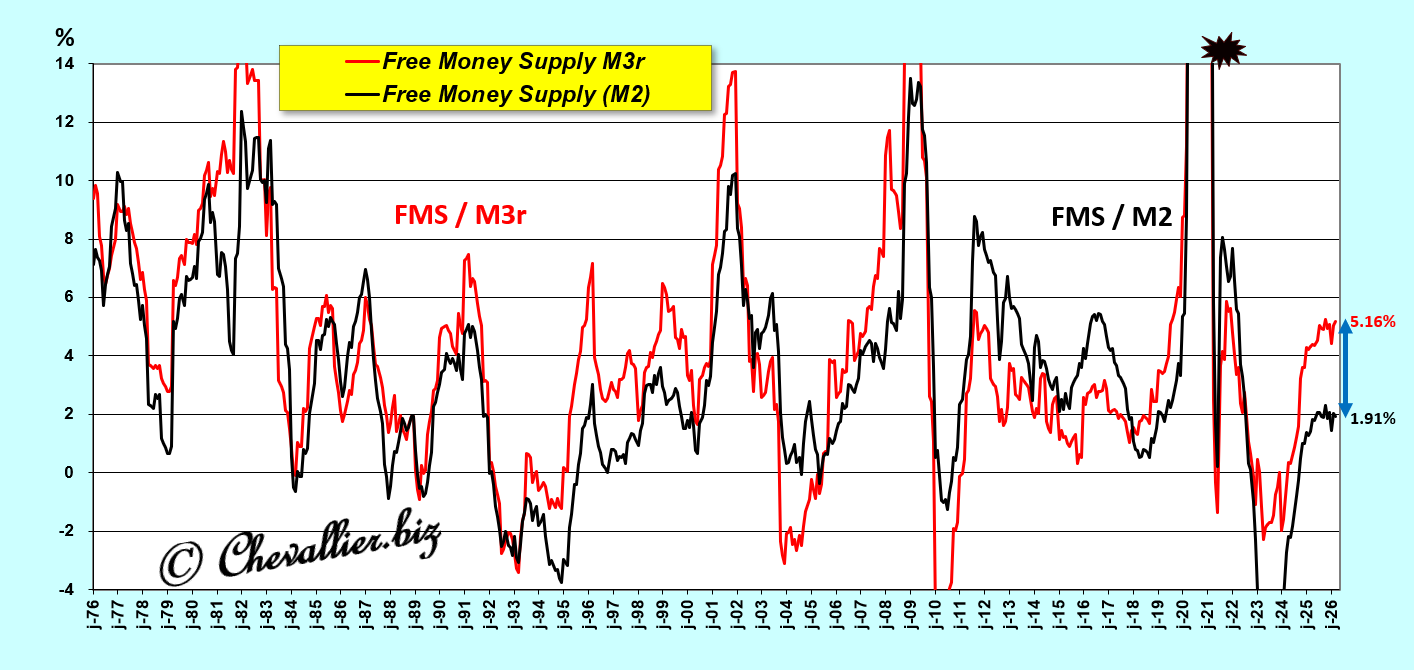

Based on these revised figures for the U.S. money supply M3r, it is quite clear—and to simplify—that an increase in this M3 money supply held by Americans leads to a decline in real GDP, and conversely, which holds true over the long term, ever since these data have been published by our friend Fred from St. Louis…

More precisely, it is the change in what I call the free money supply M3r, which is the difference between, on the one hand, the change (year-over-year in percentage terms) in the M3r money supply, and on the other hand (minus) the change in real GDP (year-over-year in percentage terms), that causes an inverse reaction in real GDP.

However, paradoxically and exceptionally, this law did not apply during the first quarter of 2026 because this free money supply M3r (Free Money Supply, denoted FMS / M3r) increased by 5.16% and real GDP growth by 2.66% (year-over-year percentage in both cases)!

Document 14:

In fact, normally, the sharp 6.0% increase in the M3r money supply at the end of March 2026 should have caused a decline in real GDP, which did not happen for two reasons…

First, the bloated M3r money supply (which corresponds to 110% of GDP, see Document 9 above) has become so large that it is beginning to create an unmanageable situation manifested by irrational market exuberance that will be short-lived and followed by a major crisis, a momentum crash.

Second, an article from ZeroHedge shows that three-quarters of the GDP growth in the first quarter of 2026 was driven by extraordinary investments in artificial intelligence, which constitutes a new bubble within the pre-existing M3 money supply bubble, one that was already too big!

Click here to read this ZeroHedge article.

Consequently, based on figures published to date and reliable supplementary estimates, the United States is in a situation of deeply entrenched monetary hypertrophy that has not occurred in the past 50 years, apart from the spike linked to the so-called covid period, which was therefore limited in time—unlike the current situation.

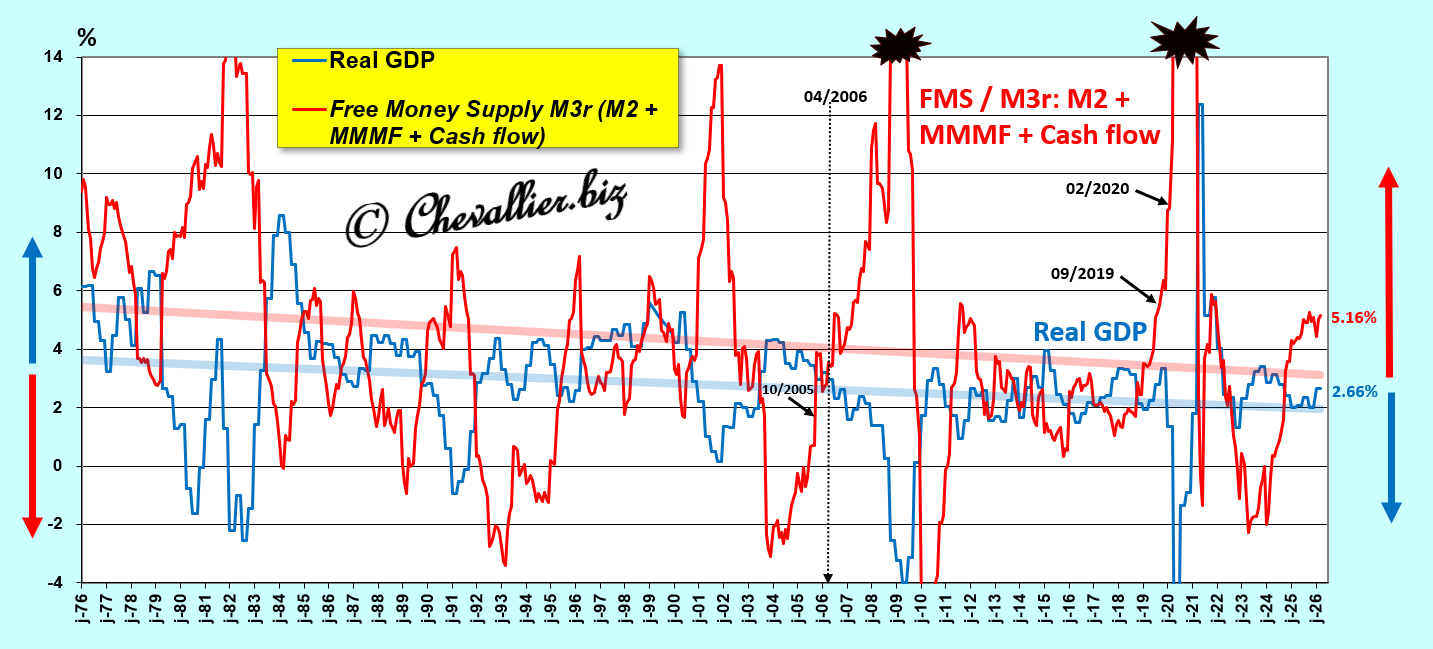

Apart from this currently completely exceptional situation, this law regarding the M3r money supply is well-verified, as shown by the arithmetic trend lines of the variations in the M3r money supply and real GDP, which are nearly parallel (slightly converging and declining), falling from around 5.5% and 4.0% in 1976 to 3.0% and 2.0%, respectively, at the end of last March,

Document 15:

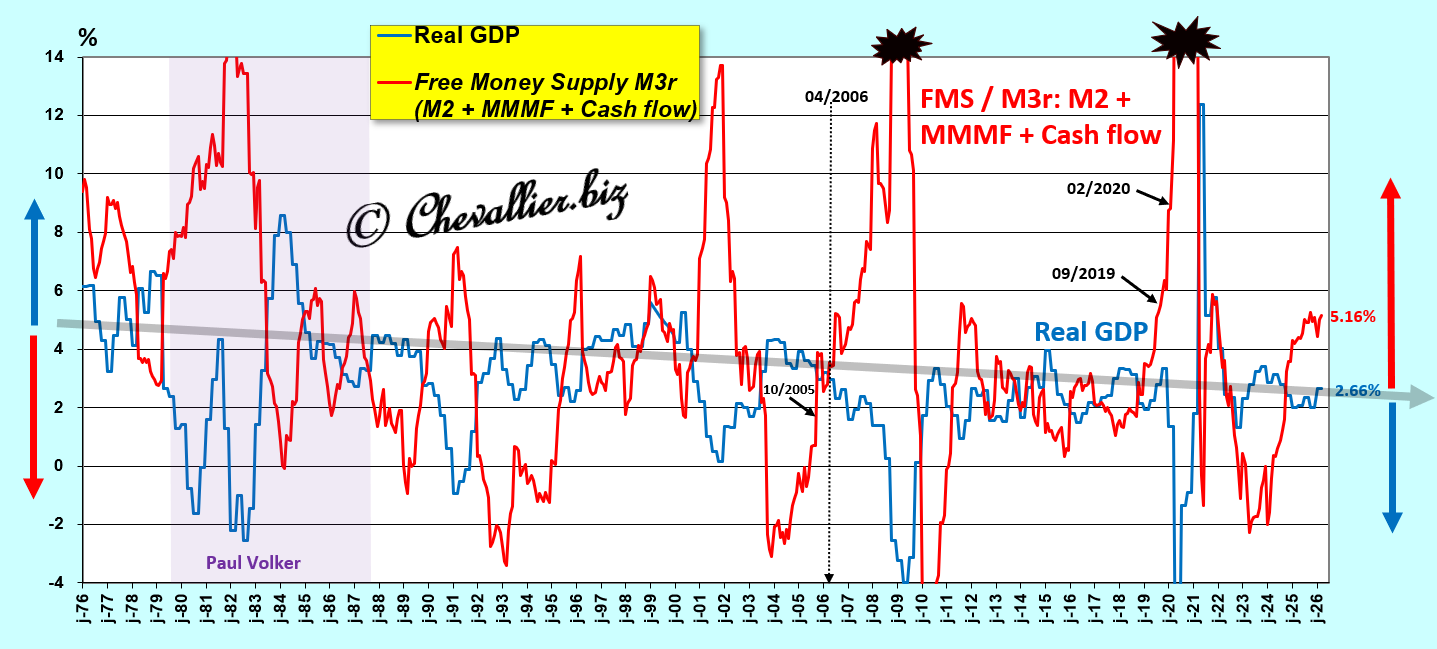

The line serving as the axis of symmetry between these curves declines from around 5.0% to 2.5% over this 50-year period, which demonstrates, among other things, that Paul Volcker managed the Fed’s monetary policy particularly well to ensure that the money supply remained sound in the United States during this period of severe financial turbulence,

Document 16:

The 5th-order polynomial trend curves clearly highlight the alternating opposition of the variations in these data,

Document 17:

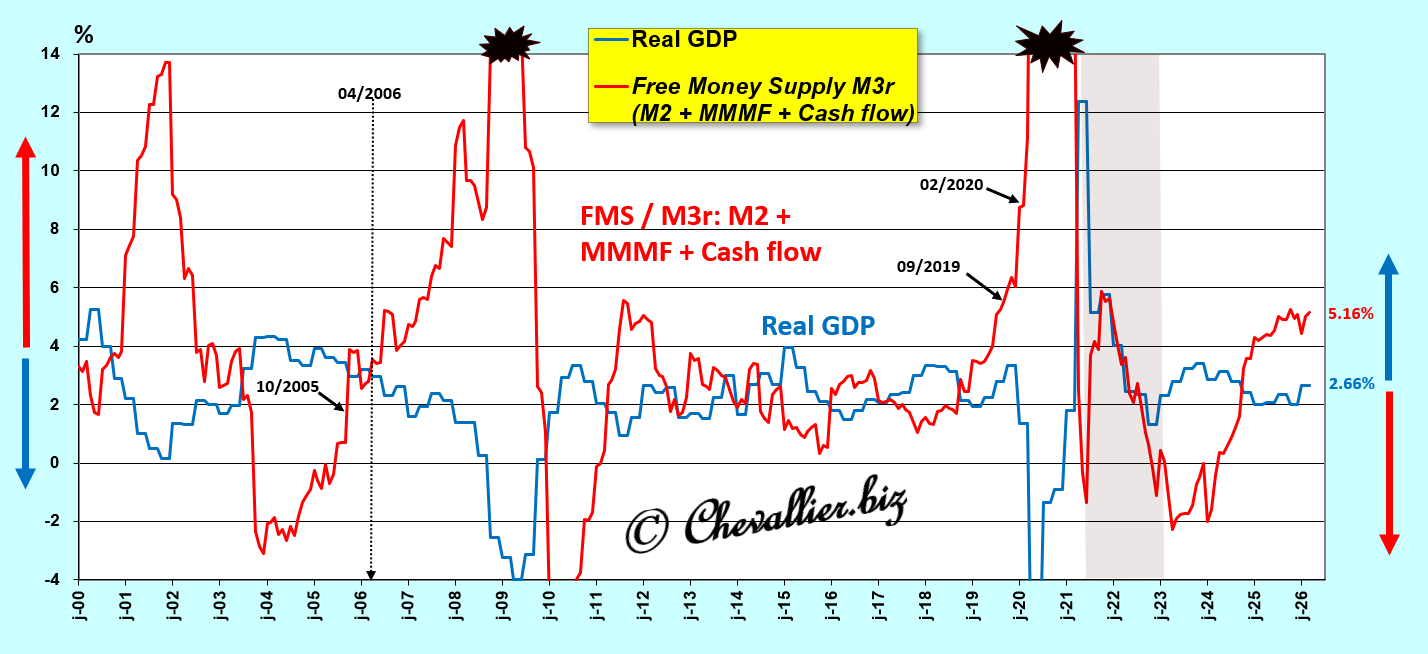

A closer look at the recent period since the early 2000s confirms that variations in the free money supply M3r continue to generate inverse variations in real GDP as before… except in the first quarter of 2026!

Document 18:

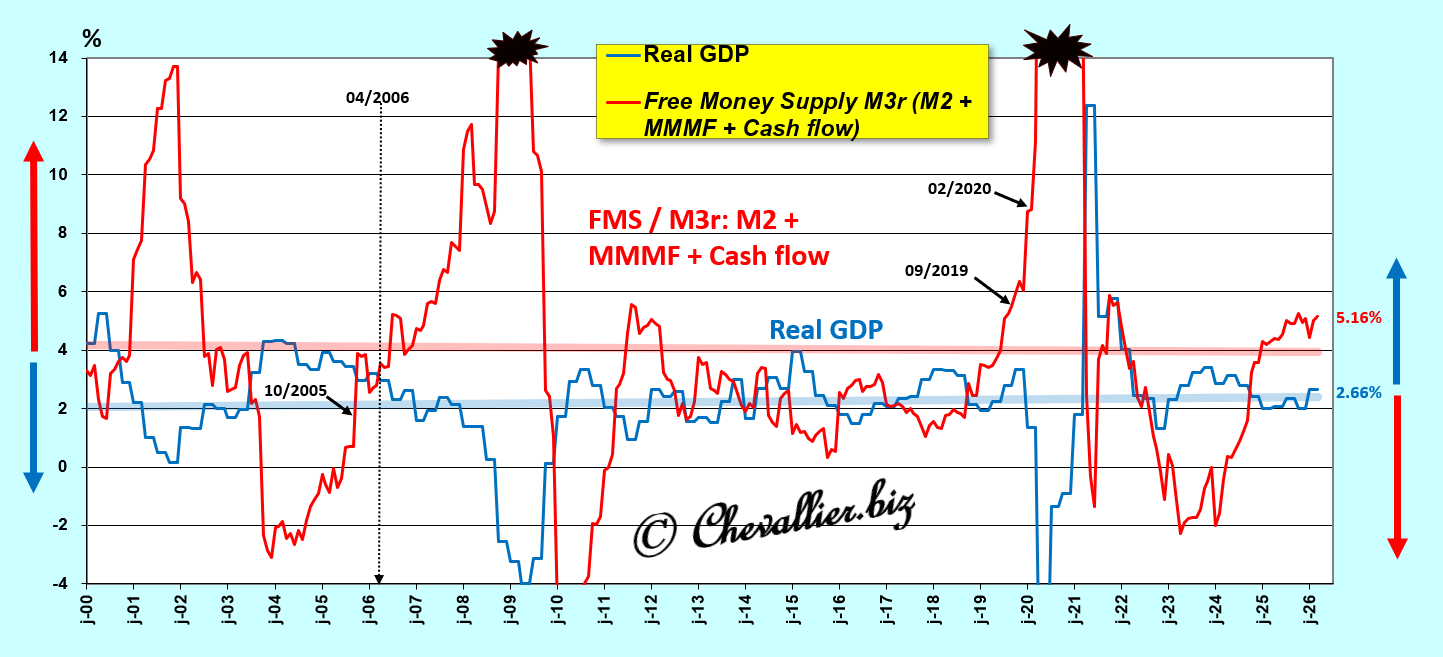

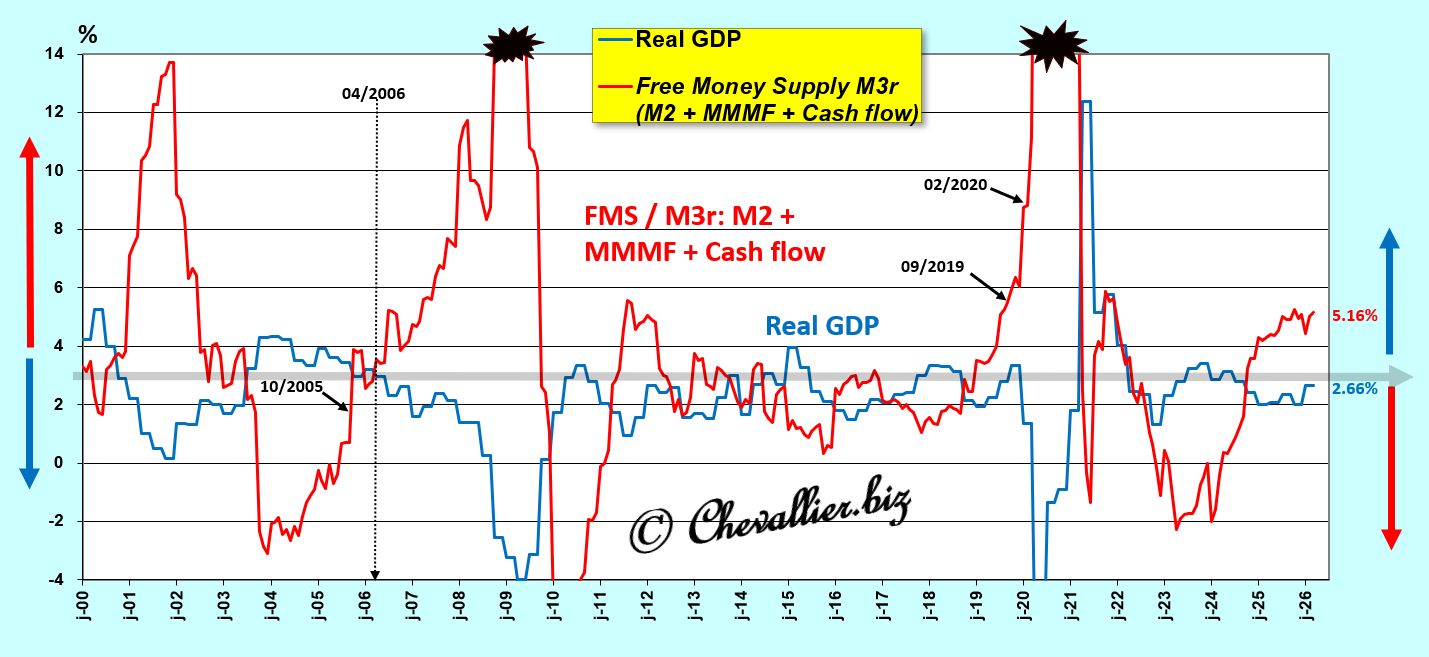

The arithmetic trend lines for the variations in the free money supply M3r and real GDP are nearly parallel (very slightly converging, and upward-sloping for GDP) and flat (horizontal), at around 4% and 2% over this recent period of the first quarter of the 21st century,

Document 19:

Logically, the line serving as the axis of symmetry between these curves is virtually stable at 3.0% over this period of the first quarter of the 21st century, which confirms the significance of this free money supply M3r!

Document 20:

This law regarding the free money supply M3r, calculated based on the total money supply of the United States, is also valid for figures pertaining solely to the monetary aggregate M2 over the long period from 1960 to the present, according to figures published monthly by the Fed…

Document 21:

… and the same holds true for the more recent period beginning in the year 2000,

Document 22:

This law regarding the broad money supply M3r calculated based on the total money supply of the United States is therefore also valid for figures pertaining solely to the M2 monetary aggregate over the long period up to the present day, according to official figures published monthly by the Fed.

However, the fluctuations observed based on the aggregate money supply M3r are of greater amplitude and occur earlier than those using figures for the M2 monetary aggregate alone,

Document 23:

It is therefore preferable to use data derived from the redefined M3r money supply, reconstructed in this manner, for analysis, as this provides the most accurate picture possible of the expected trend in real GDP growth.

***

The Pearson correlation coefficient between the trend in U.S. real GDP and what I define as the free money supply M3r is -0.78 for the period from January 2000 to March 2021, which corresponds to a very strong inverse correlation, that is, a significant relationship that, under such circumstances, is a cause-and-effect relationship.

Thus, to put it simply, it is clearly confirmed that when the free money supply M3r increases, U.S. real GDP decreases, and vice versa.

This Pearson correlation coefficient is -0.62 for the long period beginning in July 1976 and extending through March 2021.

However, this coronavirus crisis has completely and permanently disrupted the fundamental balances of America and most countries around the world, which explains a decline in this Pearson coefficient after March 2021.

Nevertheless, following this period of major turbulence, this Pearson coefficient has returned to -0.73 since January 2023.

Furthermore, the Pearson correlation coefficients calculated using the M3r money supply are virtually identical to those calculated using the M2 monetary aggregate over the same periods.

***

Analyses and conclusions regarding the impact of changes in monetary aggregates on real GDP have not been taken into account by financial market participants for the past twenty years, even though these are issues and solutions that form the basis of any nation’s economic activity.

This is precisely why Ben Bernanke took care to ensure that the Fed would no longer publish weekly figures for the M1, M2, and M3 monetary aggregates from the moment he took office as chairman of the Fed in February 2006.

Subsequently, Jerome Powell added another layer of opacity by publishing only monthly data for the M2 monetary aggregate.

Thus, only those acting within the Fed have access to this fundamental data, allowing them to manipulate financial communications and financial markets at will!

However, I have therefore managed to reconstruct the amount of the U.S. M3 money supply, denoted M3r for revised, based on the components that make up the M3-M2 aggregate, which are still published elsewhere, see my previous articles on this subject.

***

As a reminder, the M3/GDP ratio fluctuated around 70% from 1976 to the year 2000 because U.S. authorities at the time vigorously defended the discipline necessary to ensure that the U.S. monetary system adhered to this essential prudential rule, namely an M3/GDP ratio below 80%.

Document 24:

Indeed, America was then strongly committed to defending the free world against communism, which enjoyed its heyday in the 20th century, prior to the collapse of the USSR.

To this end, the necessary condition for the success of liberal capitalism was to maintain sound money under all circumstances, which was effectively achieved.

However, subsequently, the pressure exerted by financial sector leaders on U.S. authorities was so intense that they were able to develop new financial products that made their fortunes at the expense of national interests.

For example, derivatives (including CDSs) were developed in the early 2000s, and Bitcoin and cryptocurrencies from 2010 onward.

Furthermore, bank executives exerted strong pressure on monetary authorities to stop adhering to the restrictive regulations that had maintained public confidence in their banks during the second half of the 20th century.

For example, the prudential debt rule enacted by good old Greenspan—which recommended an equity ratio exceeding 10% of total debt—is now nothing more than a distant memory of a bygone era…

Another example of banking excesses: private credit, which should never have existed, is now beginning to pose major problems, even for official banks!

***

In conclusion, monetary hypertrophy (always lethal in the long run) poses a serious threat to the United States at any moment, especially in the event of exogenous disruptions—which is indeed the case at the start of 2026 with this war against Iran.

Consequently, a major, systemic crisis is brewing.

As a reminder, the first pillar of Reaganomics (and monetarism) is sound money, according to Arthur Laffer, which means that a nation must always keep its total M3 money supply within the limits of an M3/GDP ratio below 80%, which is far from the case at present!

***

The data on money market mutual funds (MMMF) are those coded MMMFFAQ027S by our friend Fred from St. Louis.

Click here to access them.

Click here to read my previous article on this subject.

Click here to read my previous article on this subject on my French website.

© Chevallier.biz