The sharp increase in the M3 money supply in the United States in February logically exacerbates the decline in real GDP growth, in accordance with my law on the free money supply.

***

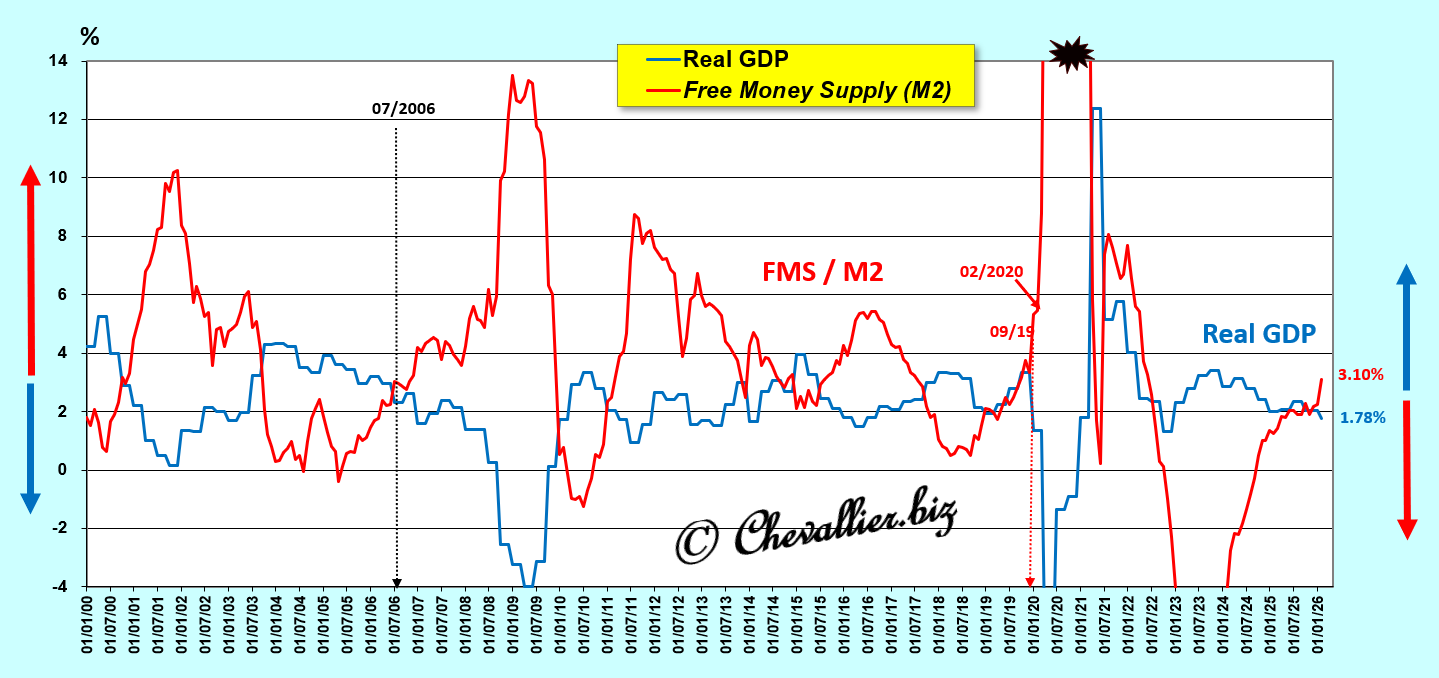

I previously posted an article online presenting my analysis of the consequences of changes in the M2 monetary aggregate on real GDP in the United States.

After reviewing the figures for the M3 money supply in the United States, I present here the effects of its fluctuations on real GDP within the framework of this law on free money supply…

To put it simply, the principle is as follows: an increase in this M3 money supply held by Americans leads to a decline in real GDP, and vice versa, which has been verified over the long term, ever since these data have been published by our friend Fred from St. Louis.

More precisely, it is the change in what I call the free M3 money supply M3r which is the difference between, on the one hand, the change (year-over-year in percentage terms) in the M3r money supply, and on the other hand (minus) the change in real GDP (year-over-year in percentage terms) that causes an inverse reaction in real GDP.

***

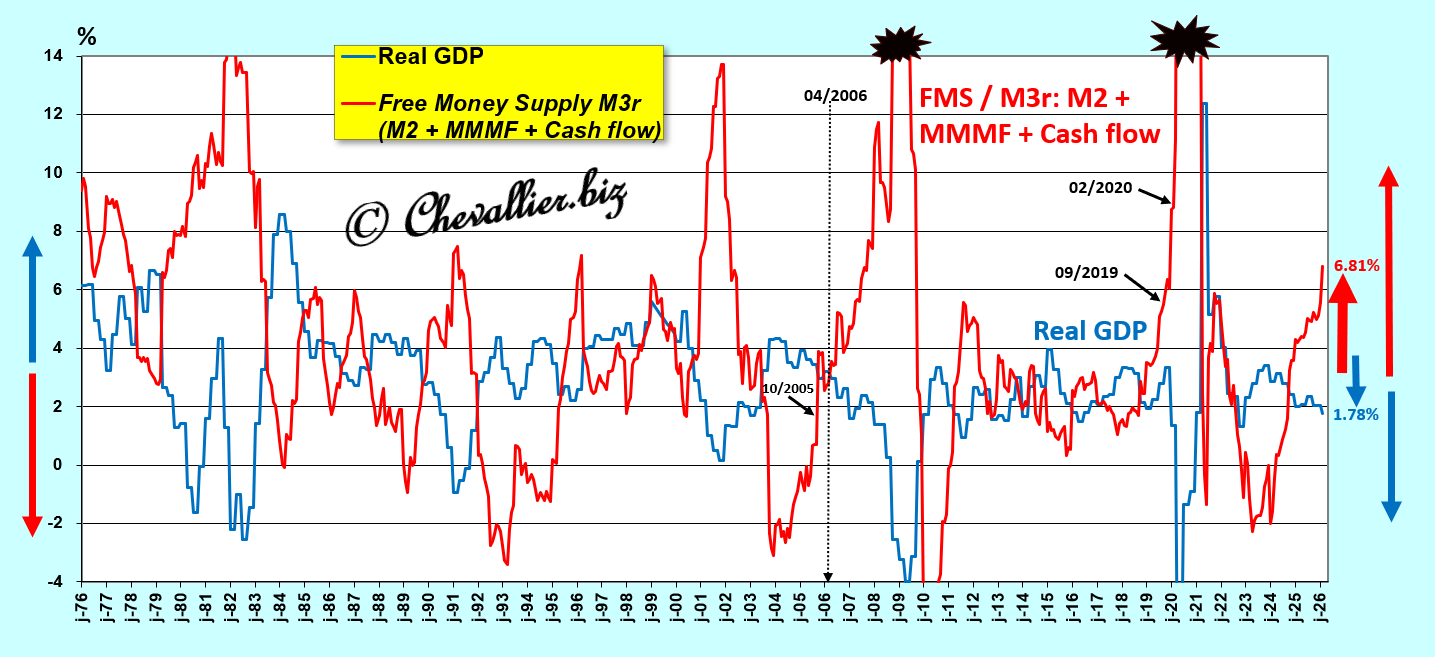

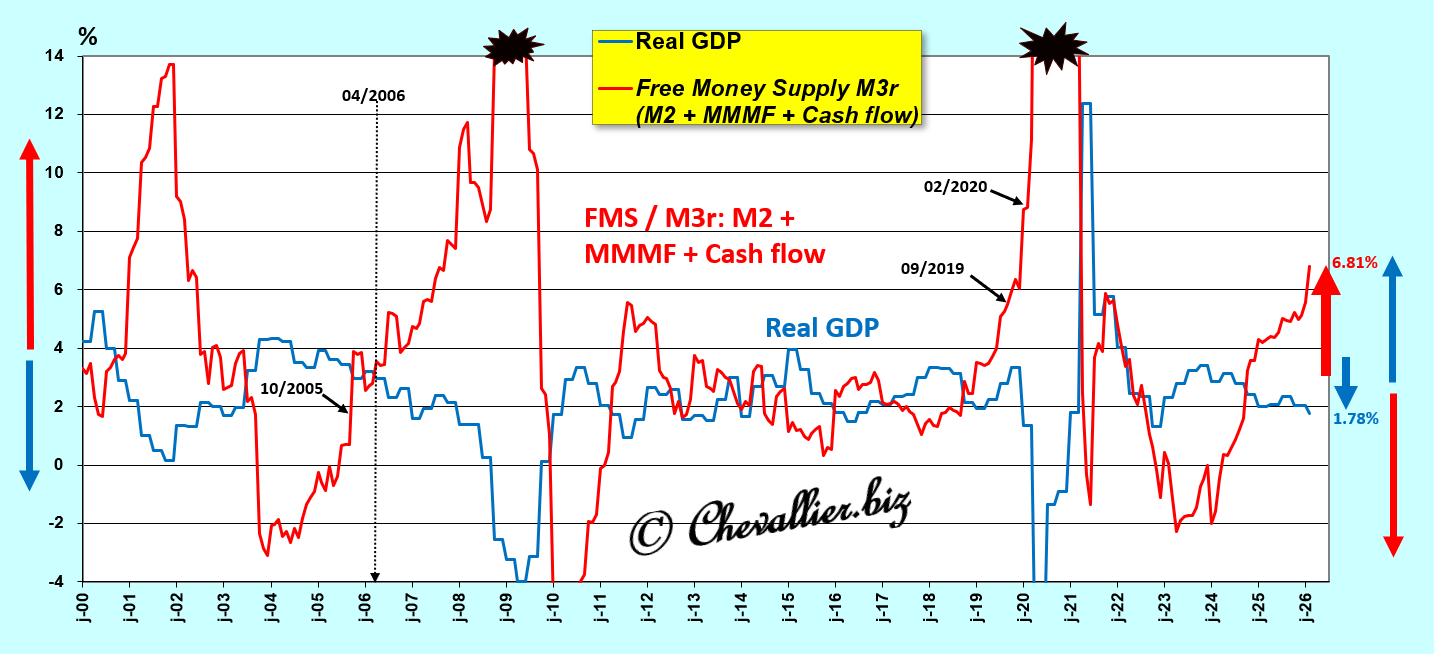

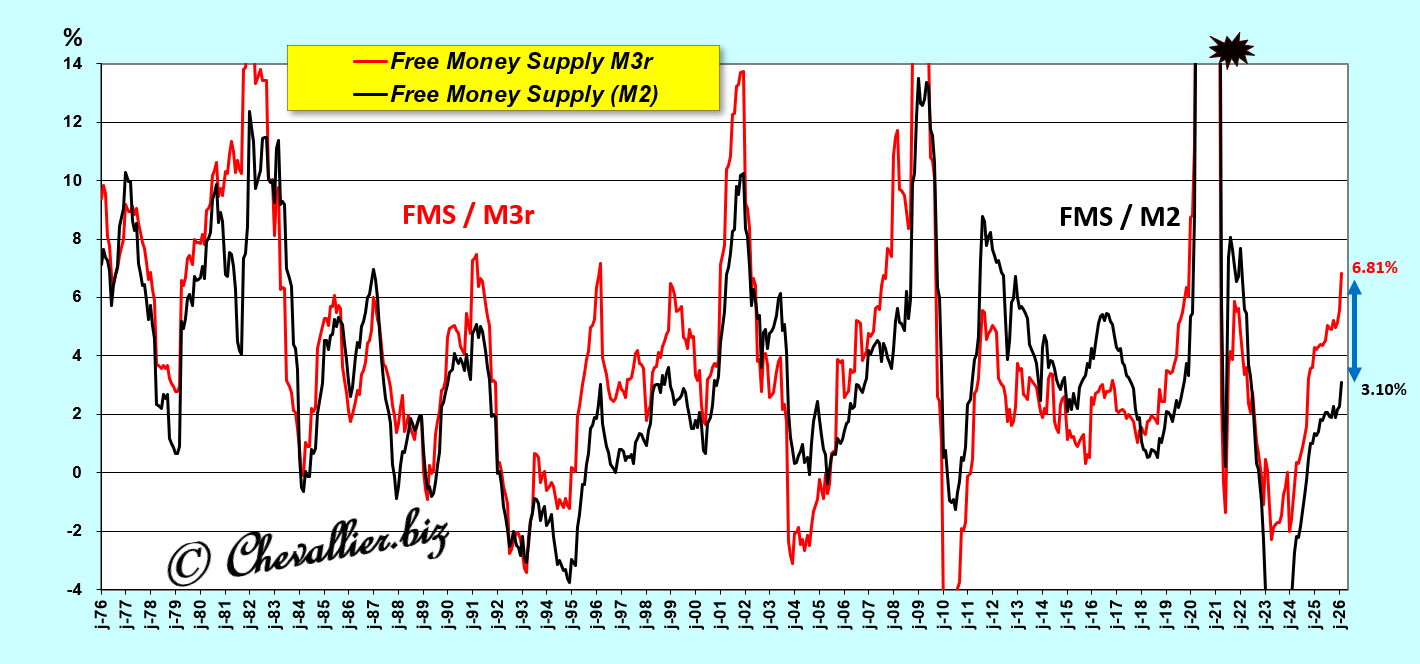

The U.S. M3 money supply increased by $398.2 billion last February, according to the latest figures published to date, causing the free money supply M3r (Free Money Supply, FMS / M3r) to jump to 6.81% and real GDP growth to fall to 1.78% (year-over-year percentage),

Document 1:

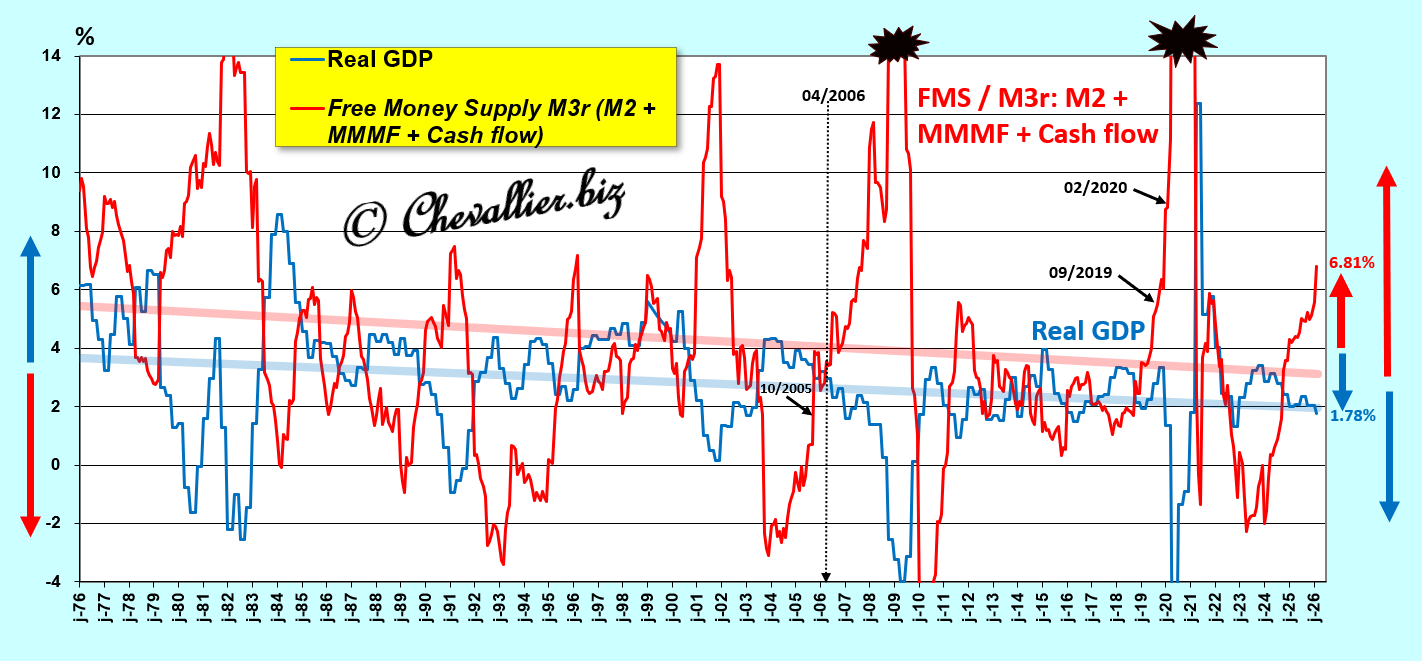

The arithmetic trend lines for changes in the free money supply M3r and real GDP are nearly parallel (slightly converging and declining), falling from around 5.5% and 4.0% in 1976 to 3.0% and 2.0%, respectively, last February,

Document 2:

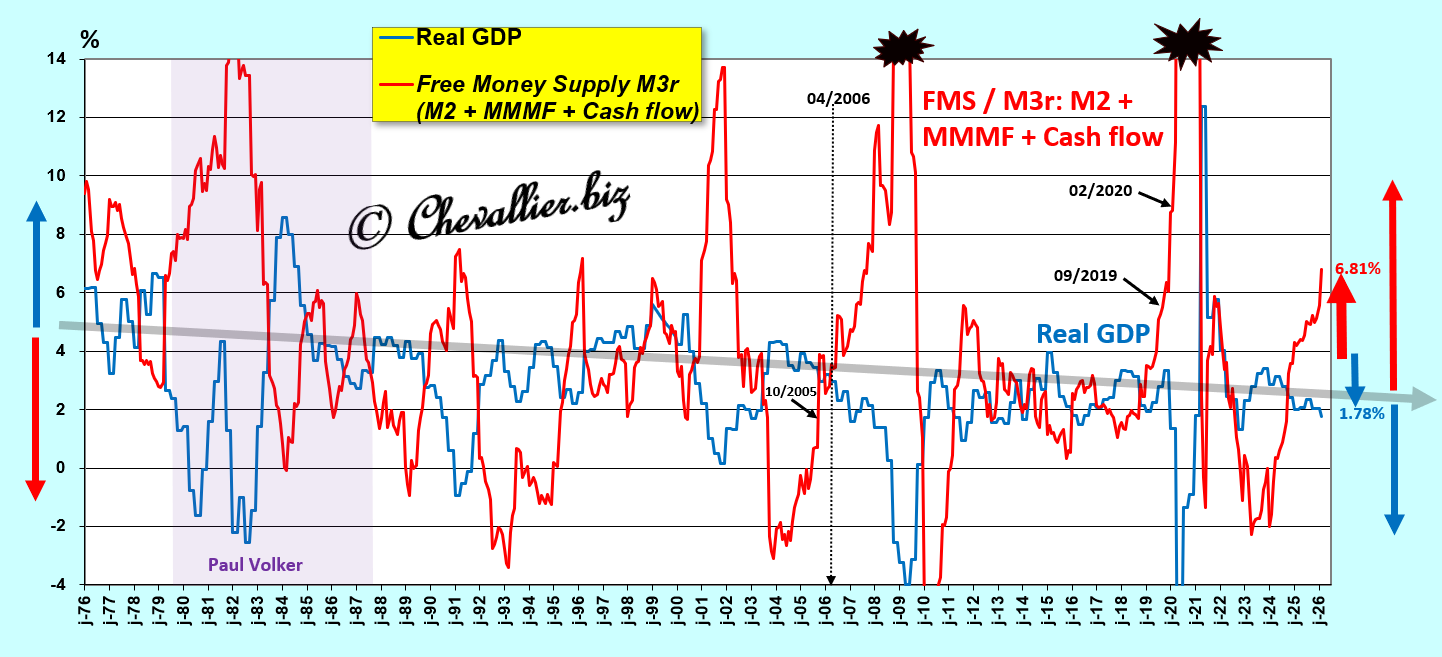

The line serving as the axis of symmetry between these curves declines from around 5.0% to 2.5% over this long 50-year period, which shows, among other things, that Paul Volcker managed the Fed’s monetary policy particularly well to keep the money supply sound in the United States during this period of severe financial turbulence,

Document 3:

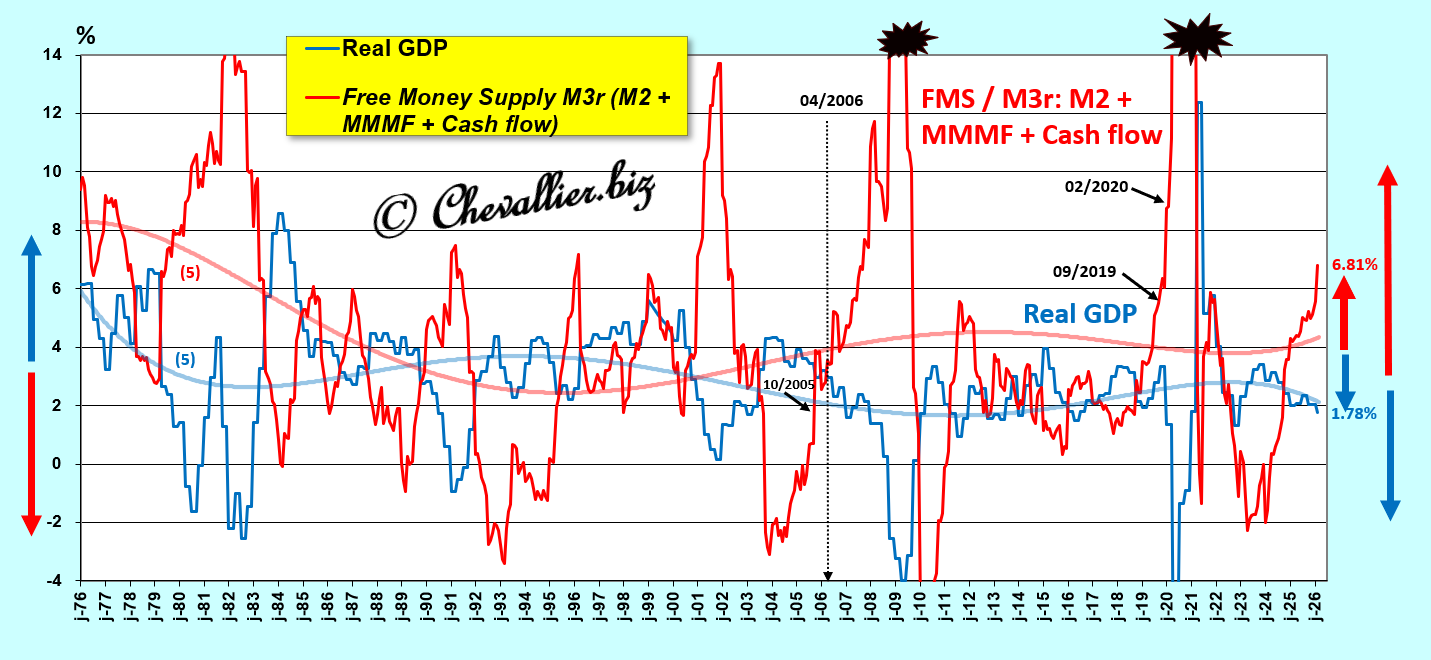

The fifth-order polynomial trend curves clearly highlight the alternating opposition of the variations in these data,

Document 4:

A closer look at the recent period since the early 2000s confirms that changes in the free money supply M3r continue to generate inverse changes in real GDP, just as before!

Document 5:

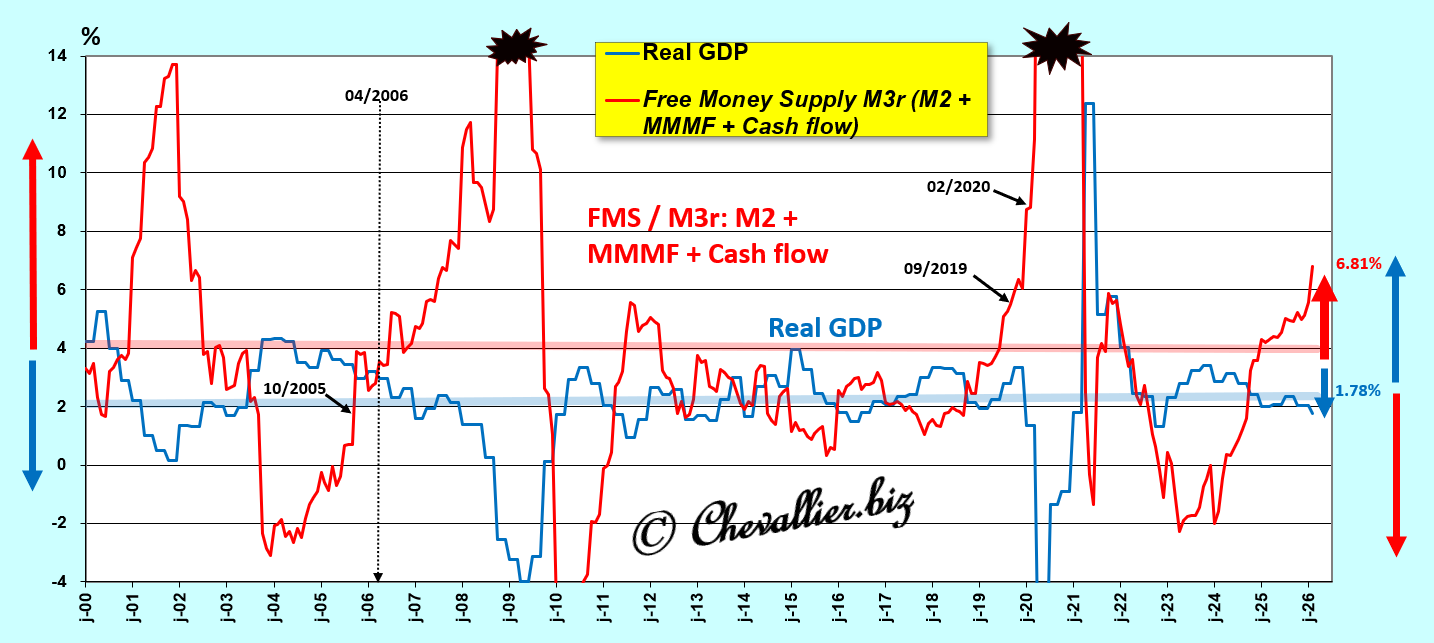

The arithmetic trend lines for the variations in the free money supply M3r and real GDP are nearly parallel (very slightly converging, and upward-sloping for GDP) and flat (horizontal), at around 4% and 2% over this recent period of the first quarter of the 21st century,

Document 6:

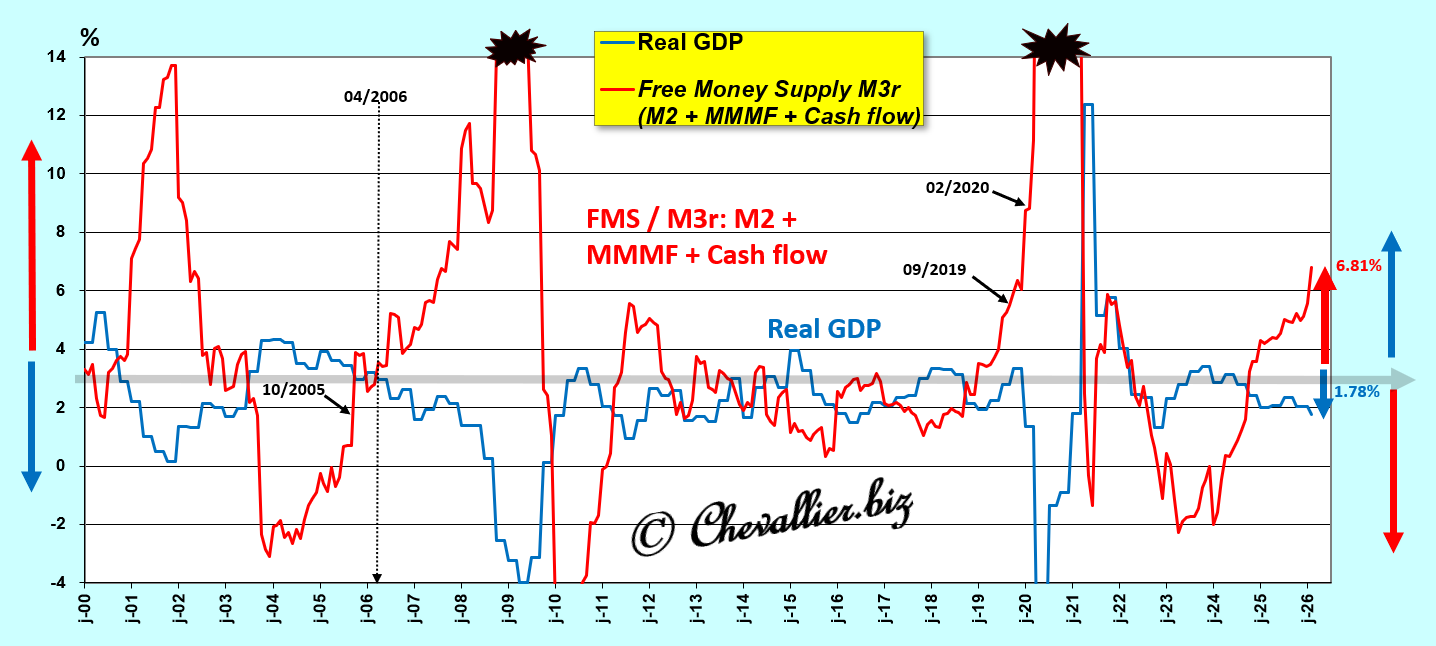

Logically, the line serving as the axis of symmetry between these curves is virtually stable at 3.0% over this period of the first quarter of the 21st century, which confirms the significance of this free money supply M3r!

Document 7:

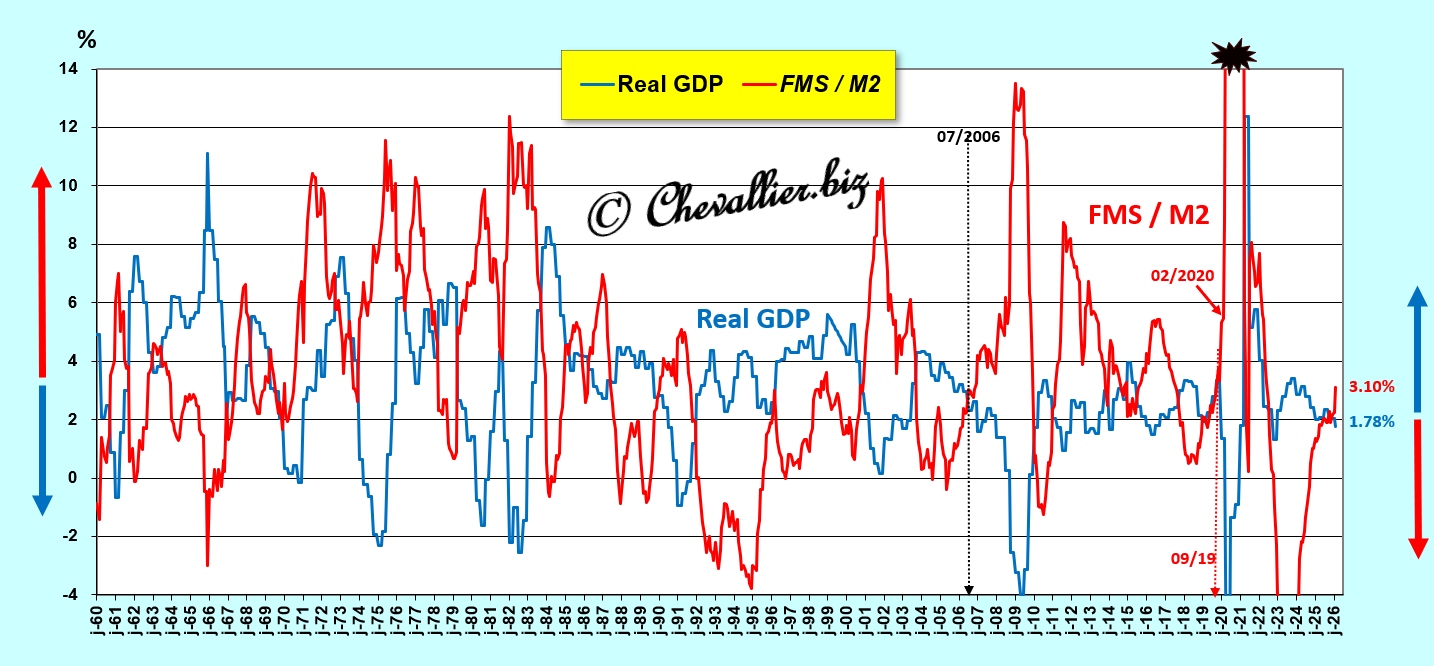

This law regarding the free money supply M3r, calculated based on the total money supply of the United States, is also valid for figures pertaining solely to the monetary aggregate M2 over the long period from 1960 to the present, according to figures published monthly by the Fed…

Document 8:

… and the same holds true for the more recent period beginning in the year 2000,

Document 9:

This law regarding the free money supply M3r calculated based on the total U.S. money supply is therefore also valid for figures pertaining solely to the M2 monetary aggregate over the long period up to the present day, according to official figures published monthly by the Fed.

However, the fluctuations observed based on the aggregate money supply M3r are of greater magnitude and occur earlier than those using figures for the M2 monetary aggregate alone,

Document 10:

It is therefore preferable to use data derived from the redefined M3r money supply, reconstructed in this manner, for analysis, as this provides the most accurate picture possible of the foreseeable evolution of real GDP growth.

***

The Pearson correlation coefficient between the trend in U.S. real GDP and what I define as the free money supply M3r is -0.68 for the period from 2000 through February 2026—the most recent figures published to date—which corresponds to a strong inverse correlation, that is, a significant relationship, in this case one of cause and effect.

Thus, when the free money supply M3r increases, U.S. real GDP decreases, and vice versa.

This Pearson correlation coefficient is -56 for the entire period under review, beginning in 1976.

***

Analyses and conclusions regarding the impact of changes in monetary aggregates on real GDP have not been taken into account by financial market participants for the past twenty years, even though these are issues and solutions that form the basis of a nation’s economic activity.

This is precisely why Ben Bernanke took care to ensure that the Fed would no longer publish weekly figures for the M1, M2, and M3 monetary aggregates from the moment he took office as chairman of the Fed in February 2006.

Subsequently, Jerome Powell added another layer of opacity by publishing only monthly data for the M2 monetary aggregate.

Only those working within the Fed have access to this fundamental data, allowing them to manipulate financial communications and financial markets at will!

However, I have managed to reconstruct the amount of the U.S. M3 money supply, denoted M3r for revised, based on the components that make up the M3-M2 aggregate, which are still published elsewhere, see my previous articles on this subject.

***

The data on money market mutual funds (MMMF) are those coded MMMFFAQ027S by our friend Fred from St. Louis.

Click here to access them.

The data for money market mutual funds (MMMF) and for Corporate net cash flow (CNCF) for the fourth quarter of 2025 are those published by the authorities and reported by our friend Fred from St. Louis. For the first two months of 2026, the data are estimates extrapolated from previous quarters.

Click here to read my previous article on this subject.

Click here to view this article on my website in French.

© Chevallier.biz