Abstract

Monetarists and nearly all economists agree that an increase in a nation’s money supply causes inflation, which stimulates GDP growth, and that, conversely, a decrease in the money supply leads to a decline in GDP, as was the case, for example, during the Great Depression of 1929.

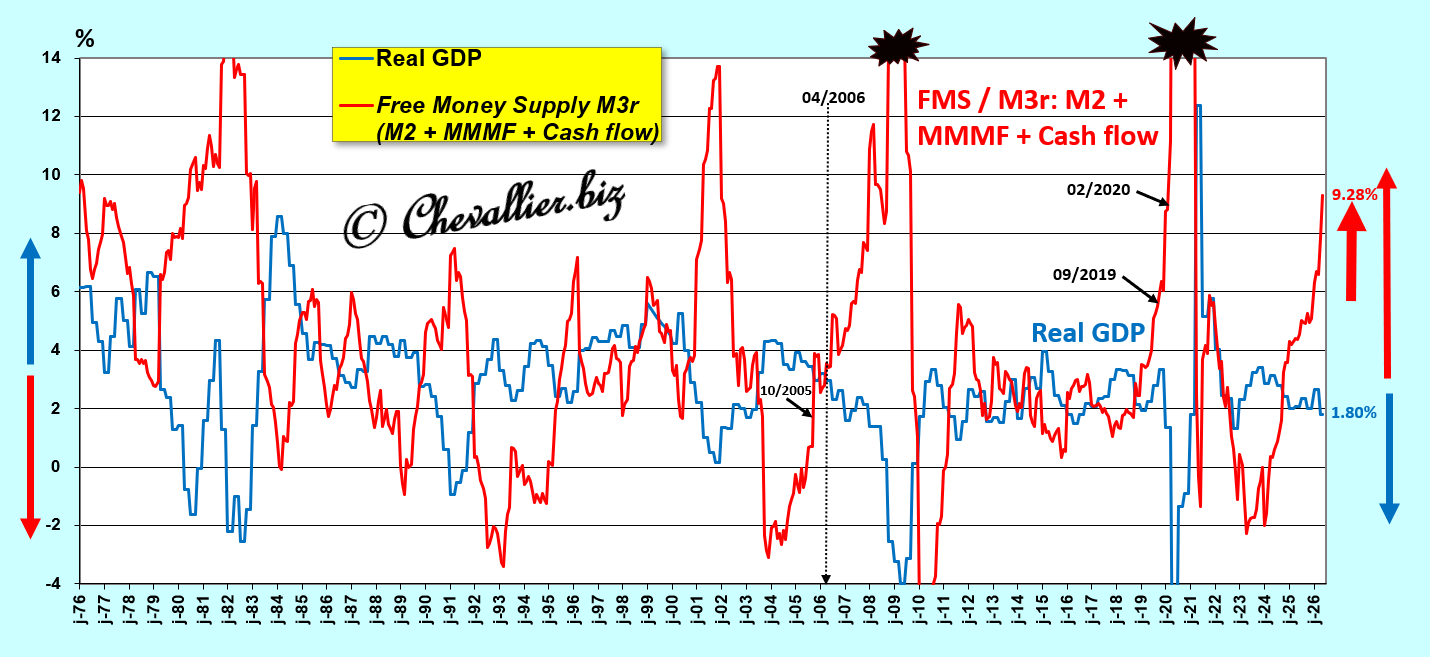

However, an examination of official time series data on the evolution of the money supply and GDP in the United States since the postwar period shows that these assertions do not correspond to reality.

Indeed, it becomes clear that an increase in the U.S. M3 money supply leads to a decline in real GDP, and vice versa.

My analyses and conclusions based on this law of free money supply therefore contradict the studies published on this subject, but they are grounded in the observation of indisputable real-world data.

Consequently, the entire body of economic and monetary theory must be rethought.

Will the economic community be willing to question its dogmas?

E pur si muove

***

Studies on the relationship between changes in a nation’s money supply and changes in GDP were conducted primarily in the 20th century, but they were based on theoretical debates rather than on observations of data spanning long periods.

The arguments and reasoning put forward by economists might have seemed logical and coherent, with differences of opinion and controversies fueling debates among various schools of thought.

At the dawn of the 21st century, we now have reliable and easily accessible databases (such as the FRED database from the St. Louis Federal Reserve Bank) that allow us to study and identify cause-and-effect relationships on this subject and to rationally resolve these issues on indisputable grounds that can be described as scientific, since these solutions are sourced, verifiable, and reproducible.

However, to understand what might appear to be paradoxical—and thus contrary to conventional wisdom—namely that an increase in the U.S. M3 money supply leads to a decline in real GDP, and vice versa, one need only revisit the principle of edifying stories as imagined by 19th-century economists, such as Eugen von Böhm-Bawerk, who explained the basics of economics to his contemporaries—who were largely uneducated farmers—in the following way…

Consider a farmer who comes down from the mountains on Saturday morning to sell about a hundred of his cheeses at the village market.

By noon, he has sold everything, and his cash box is full of bills and coins, which he spends entirely at local shops on his family’s and farm’s weekly needs.

But last week, at 10 a.m., since he had sold only a small portion of his cheese, he lowered his prices. By noon, he still had unsold cheese and far less money than he had at the same time the previous week.

Why? The answer is simple: he was told that the government was going to impose new taxes because a war might break out.

So the villagers began to set money aside. Some of them bought only half a cheese, while other regular customers didn’t buy anything at all, and so on.

So this farmer, too, set money aside and spent less at other merchants’ shops.

In conclusion, a vicious cycle was set in motion: the money supply increased (due to these precautionary savings that are no longer circulating), which led to a decline in wealth creation by and for everyone—and thus in GDP.

And this is exactly what just happened in the United States in April and May: Americans have set money aside over the past two months, causing the M2 money supply to jump by… 366 billion dollars; as demand fell, the sales of many businesses also declined, and the same will therefore be true for a large portion of GDP.

However, this decline in GDP has not yet materialized (in the first quarter of 2026) because exceptional investment spending on artificial intelligence is stimulating overall growth, and this phenomenon is independent of changes in the money supply.

Furthermore, with regard to the components of the monetary aggregate M3-M2, the peak of the monetary bubble created by COVID-19 continues to fuel an excess of money in circulation, which compounds the financial excesses that began after the end of the Cold War.

As a result, a multitude of financial products have proliferated, even though monetary authorities should have regulated them—and in some cases, banned them.

For example, cryptocurrencies are not currencies but Ponzi schemes; derivatives should have been restricted; the big banks too big to fail should have been broken up, just as AT&T’s Baby Bells were; banks should have adhered to prudential debt rules, as Alan Greenspan advocated; and so on.

After the fall of communism in the USSR and China, America no longer needed to maintain sound money because it no longer had any dangerous adversaries.

The financial sector took advantage of this to profit on all fronts, which led to this historic monetary hypertrophy.

Only a major crisis—worse than that of 1929—could bring it to a head, which would allow for the restoration of sound money in the United States, and this is precisely what is currently brewing as a result of this monetary expansion.

***

Friedrich Hayek is the only economist who fully understood that an undue increase in the money supply could only lead to a decline in GDP—and vice versa—though he failed to provide the proper justifications for this.

The same was true of some of Ludwig von Mises’s work.

Click here to read my article on my French-language website.

© Chevallier.biz