An unprecedented monetary hypertrophy has taken place in the United States over the past two decades, which always has fatal consequences in the long run…

It has been caused, on the one hand and above all, by an increase in the supply of Eurodollars—that is, dollars (USD) circulating outside the United States (and especially petrodollars)—with no connection to the wealth created there, and on the other hand by financial entropy leading to growing turmoil.

The bursting of this monetary bubble can only occur through the absorption of these Eurodollars and a return to adherence to fundamentals in the financial and banking sectors.

The major problem is that U.S. political leaders, who have no monetarist background, are convinced that it is this mass of Eurodollars that allows them to maintain their global hegemony, whereas in reality it is the root cause of their loss of power and influence in the world, as well as their fundamental economic and monetary problems.

Domestically, American financial circles have developed financial products that should never have existed or that need to be regulated (and the same is true in so-called Western countries), yet they oppose any return to a sound financial environment.

***

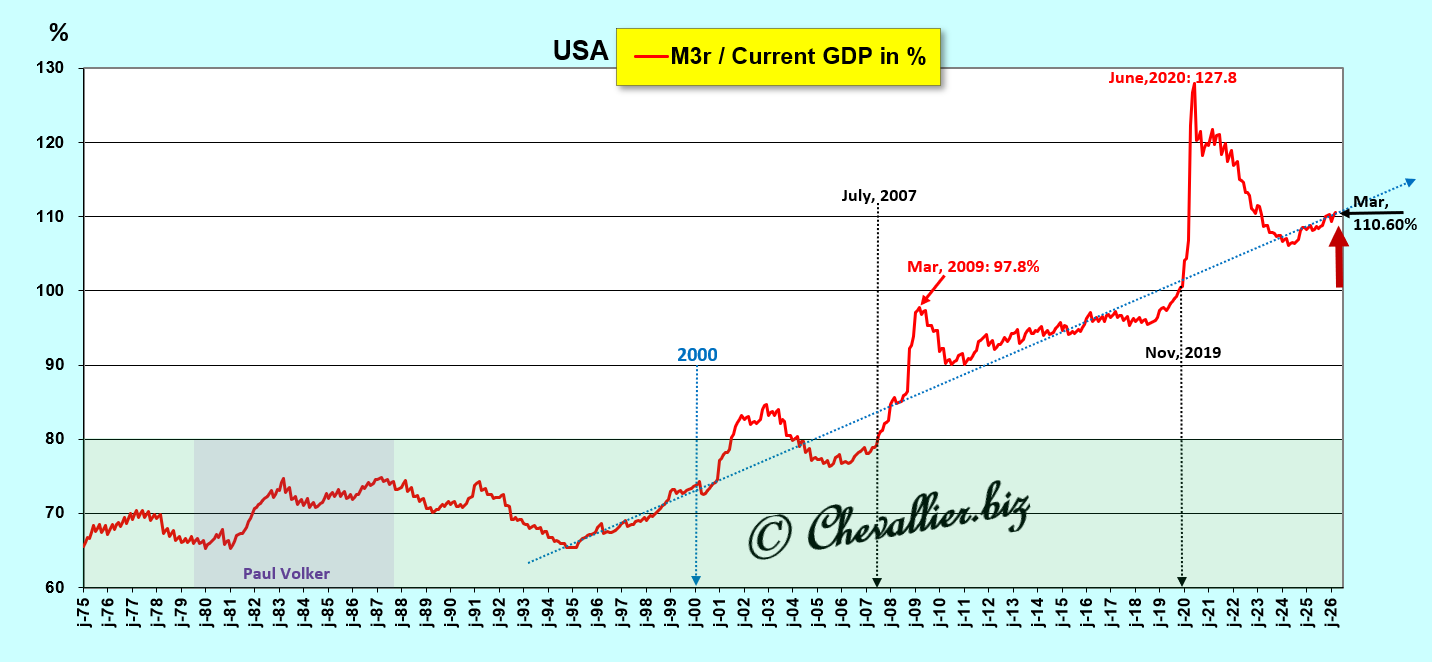

The monetary hypertrophy that has developed in the United States over the past twenty years is clearly evident in the graph showing the evolution of the share of the U.S. M3 money supply relative to annual current GDP (as a percentage).

This ratio, M3/GDP, should always remain below 80%, yet it has far exceeded this critical threshold since July 2007, reaching a first peak in March 2009 in connection with the Great Recession, then an all-time high in June 2020 amid this coronavirus crisis, and it continues to rise along its long-term upward trend, whereas it normally fluctuated around 70% during the last quarter of the 20th century!

Document 1:

After World War II, U.S. authorities intervened to firmly contain this M3/GDP ratio within an optimal fluctuation band of around 70% until the end of the 20th century, that is, throughout the entire Cold War period, as it was then imperative for America to maintain its leadership status over the free world and for Western European countries to enjoy strong growth in the face of communist nations led by the USSR.

Subsequently, that is, since the year 2000, dysfunctions in the U.S. financial system began to emerge: the M3/GDP ratio then departed from its optimal fluctuation band—centered at 70%—to continue on a long-term upward trend through the most recent data published to date, meaning that this expansion continues to grow inexorably.

The U.S. M3 money supply remained within normal limits, fluctuating around 70% of annual GDP at the end of the 20th century, because the U.S. financial system was then operating in accordance with rules established by competent authorities who could enforce them in the face of ill-advised initiatives by certain market participants (including the banksters), which was no longer the case thereafter, that is, since the early 2000s.

If this prudent management of the U.S. M3 money supply had continued to the present day, M3 would have amounted to 22,300 billion dollars, compared to 35,232 billion dollars at the end of last March (according to standard calculations, using the M3/GDP ratio of 70%), meaning that this excess money supply amounts to approximately… 12,932 billion dollars!

Document 2:

As I have written previously, this monetary bloat was caused by the development of multiple dysfunctions within the U.S. financial system, and more broadly within so-called Western countries.

This is how new financial products developed that were poorly regulated, such as derivatives, CDSs, cryptocurrencies (which are based on a Ponzi-style scheme), and recently so-called private loans—that is, outside of banks—which, incidentally, no longer comply with the prudential rules that should still apply, etc.

Furthermore, the unconventional management of the federal government’s cash reserves and the Fed’s assets contribute to fueling this bloated M3 money supply in the United States (see my articles on this subject).

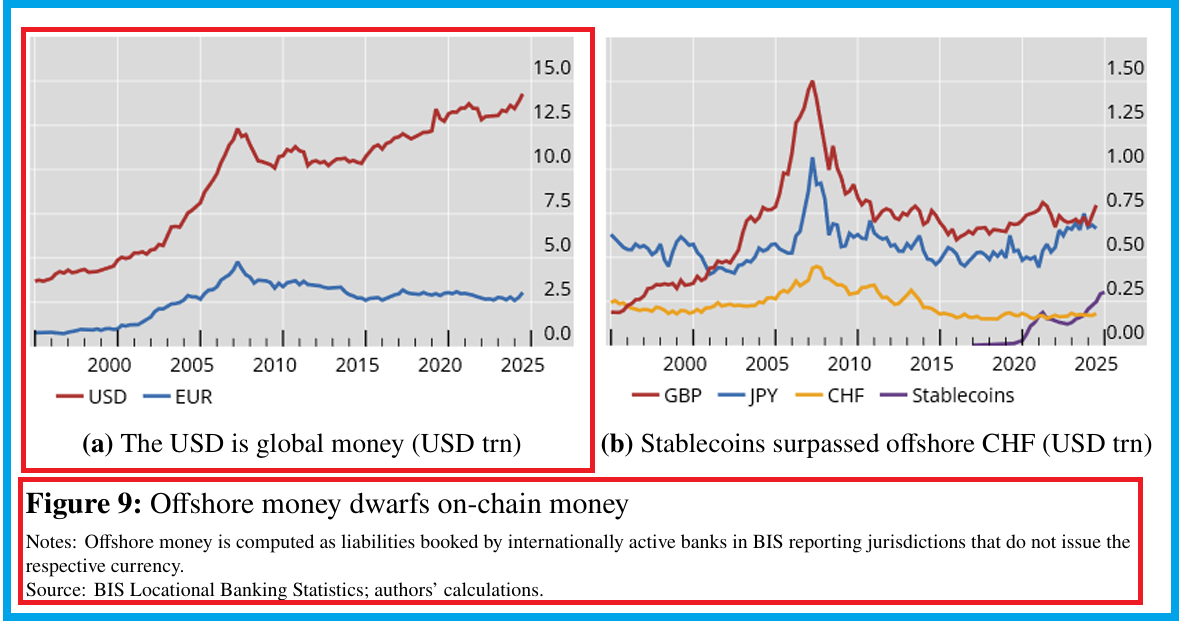

Eurodollars, originating in part from petrodollars, constitute another significant source of this monetary bubble that I had not previously identified…

According to a reliable study (on another subject) conducted by Iñaki Aldasoro, Jon Frost, and Hiro Ito for the Bank for International Settlements, the volume of these Eurodollars is projected to reach… 14,000 billion dollars by 2025,

Document 3:

This volume of Eurodollars is said to have tripled since the early 2000s (Figure 9a),

Document 4:

A large portion of these Eurodollars lacks legitimacy because they circulate with no connection to wealth creation in the United States (GDP).

This is a major source fueling the monetary bloat plaguing the United States, and monetary bloat always has lethal consequences in the long run, as demonstrated, for example, by France with the Mississippi Bubble created by Law’s bank in 1720 and by Germany during the interwar period.

From the establishment of the Bretton Woods system in 1944 until the end of the 20th century, Fed officials consistently succeeded in keeping the money supply within its optimal fluctuation range by maintaining the M3/GDP ratio at around 70%.

When inflationary pressures threatened to gain momentum, FOMC members raised the Fed’s base rate, which then triggered a recession and a decline in the M3/GDP ratio.

Thus, Ben Bernanke raised the Fed’s benchmark rate, triggering the Great Recession, which had the advantage of bursting part of the monetary bubble and restoring some of the fundamentals in the financial sector; however, this measure failed to bring the money supply back within its normal fluctuation band—that is, with an M3/GDP ratio below 80%.

Subsequently, Jerome Powell raised the Fed’s benchmark rate to a range of 5.25% to 5.50% on July 26, 2023, which brought inflation back into a potentially acceptable range; however, this measure had no positive effect on curbing monetary expansion, as it far exceeds what could still be considered acceptable,

Document 5:

Thus, for the first time since the 1950s, raising the Fed’s benchmark rate is no longer sufficient to restore monetarist fundamentals in the United States!

Indeed, to burst this American monetary bubble, it would be necessary to implement two types of drastic measures…

First, financial and monetary authorities must absolutely require the leaders of financial institutions to comply with international accounting standards and sound prudential management rules, as was the case during the second half of the 20th century.

For example, Jamie Dimon should no longer be able to publicly state that if a bank must be declared bankrupt due to regulation, that regulation must be changed and the “banksters” must be “left alone”!

Second, political authorities should put an end to the United States’ untimely interventions in the rest of the world in order to reduce the volume of Eurodollars there.

Indeed, a cost-benefit analysis would show that the costs of official U.S. military interventions from 800 bases spread across the globe and of operations that are more or less well concealed far outweigh the perceived benefits.

The model based on empires—British, French, and, in earlier times, Spanish and Portuguese—plundering the resources of what was once the Third World has long since passed, even in renewed forms, as evidenced by the fact that annual military spending, currently exceeding $1 trillion, is greater than the U.S. trade deficit, which has exceeded $1 trillion (over a full year) since the beginning of 2022.

Document 6:

Furthermore, the U.S. dollar (USD) should no longer be used by entities in other countries for payments between themselves.

For example, when Chinese companies purchased hydrocarbons from Russian exporters, the contracts stipulated payment in USD instead of using the currencies of the countries involved, such as rubles or yuan.

International tensions and even recent wars have had the advantage of putting an end to these anomalies and thus beginning to reduce the volume of Eurodollars previously used for these international payments, but this is not enough to bring the M3/GDP ratio back below the critical 80% threshold!

***

Conclusion: as I wrote at the beginning of this article, the major problem is that U.S. political leaders, who have no monetarist background, are convinced that it is this mass of Eurodollars that allows them to maintain their global hegemony, whereas in reality it is the root cause of their loss of power and influence in the world, as well as their fundamental economic and monetary problems.

It is unlikely that U.S. political leaders will ever understand these problems, and it is even less likely that they will implement the necessary solutions.

The fact that Ben Bernanke discontinued the publication of M3 money supply figures as soon as he took office as Fed Chair suggests that Fed economists—who clearly have a strong monetarist background—have conducted analyses reaching the same conclusions as mine, yet they have never made them public.

The wars in Ukraine and the Middle East, the dysfunctions in the banking, monetary, and healthcare systems (with COVID), in the stock markets with artificial intelligence, etc., are exacerbating global turmoil—which is also the objective of certain networks operating covertly but effectively…

It is difficult to imagine that Kevin Warsh could fundamentally resolve these core monetarist problems, but it is not impossible.

This war against Iran may have had as its main (and well-concealed) objective the elimination of a large portion of these Eurodollars (especially those derived from petrodollars) for the greatest benefit of the American multi-billionaires linked to Israel…

***

Click here to access the BIS study page estimating the amount of Eurodollars.

Click here to read the article on this subject.

Click here to read this article on my website in French.

© Chevallier.biz