- A form of monetary hypertrophy that is ultimately lethal has developed in the United States.

- No solution is conceivable that would deflate it without causing catastrophic damage.

- Kevin Warsh can only prevent this monetary hypertrophy from worsening.

***

The second half of the 20th century was dominated by the Cold War, that is, by the debates and conflicts between communism and liberal capitalism. Over the course of those decades, more and more countries around the world, especially among the so-called developing nations, joined the camp of the so-called communist countries. The United States was then regarded as the ultimate defender of the Free World.

U.S. leaders therefore felt compelled to intervene around the world to defend this Free World. To achieve this goal, they had to maximize their own economic performance in order to strengthen their financial—and thus military—power, by demonstrating that liberal capitalism was the best solution for optimizing the wealth of nations and their inhabitants.

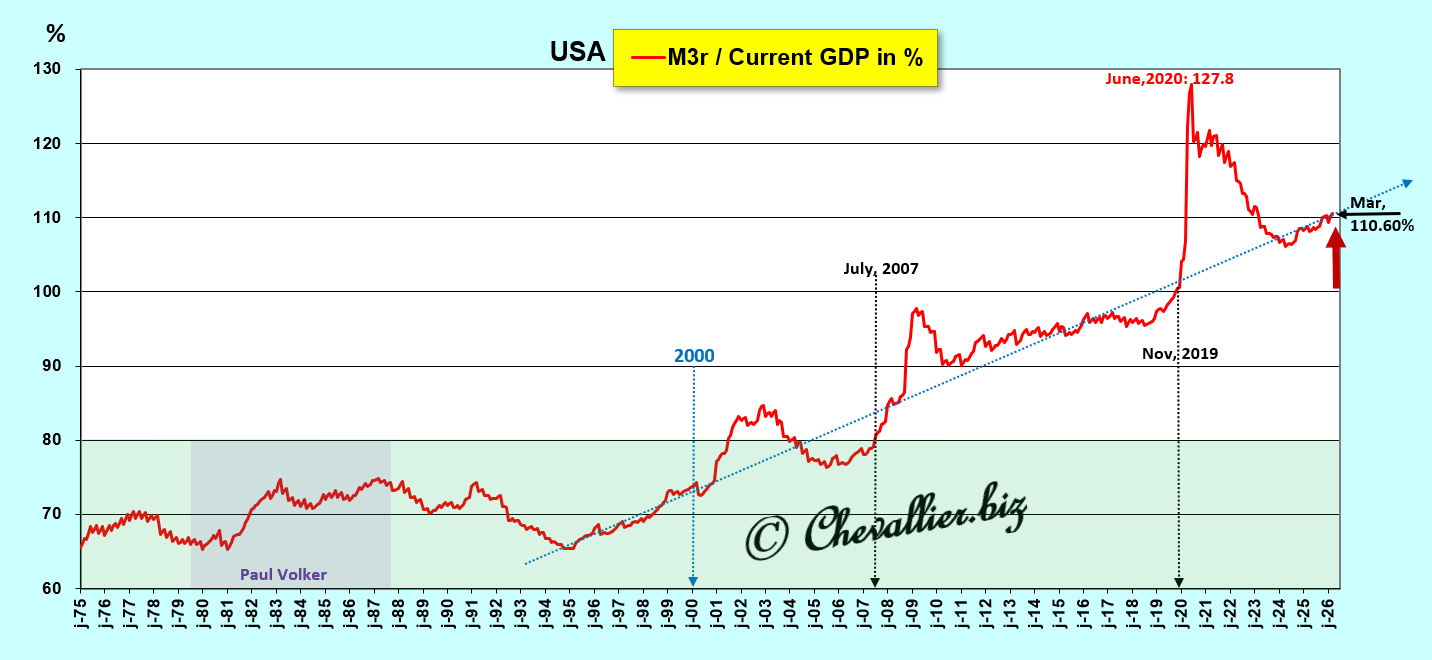

U.S. leaders believed at the time that the success of this economic policy depended primarily on the monetary policy conducted by the central bank, which had to strictly contain the growth of the M3 money supply so that it did not exceed the critical threshold of 80% of current GDP (see my articles on this subject), and this was achieved thanks, among other things, to the monetary policy pursued by Fed leaders following the 1944 Bretton Woods Conference.

The first pillar of Reaganomics is a sound currency, according to Arthur Laffer

Document 1:

Unfortunately, after the long-awaited collapse of the USSR, this fundamental monetary discipline was abandoned under pressure from the U.S. financial sector, a trend that began to manifest itself in the Great Recession of 2008.

Subsequently, other ill-timed interventions exacerbated this monetary hypertrophy, especially in connection with this coronavirus situation.

Yet history teaches us that any monetary hypertrophy always has catastrophic consequences, as demonstrated, for example, by France with the Mississippi Bubble created by Law’s Bank in 1720 and by Germany in the interwar period.

The biggest problem we face today is that those who manipulate financial markets and public opinion—and who hold the world’s primary powers—have skillfully obscured these fundamental monetary issues so that no one (or almost no one!) can analyze them and draw the necessary conclusions—conclusions that would, however, allow for the restoration of sound fundamentals and thus prosperity in the United States and around the world.

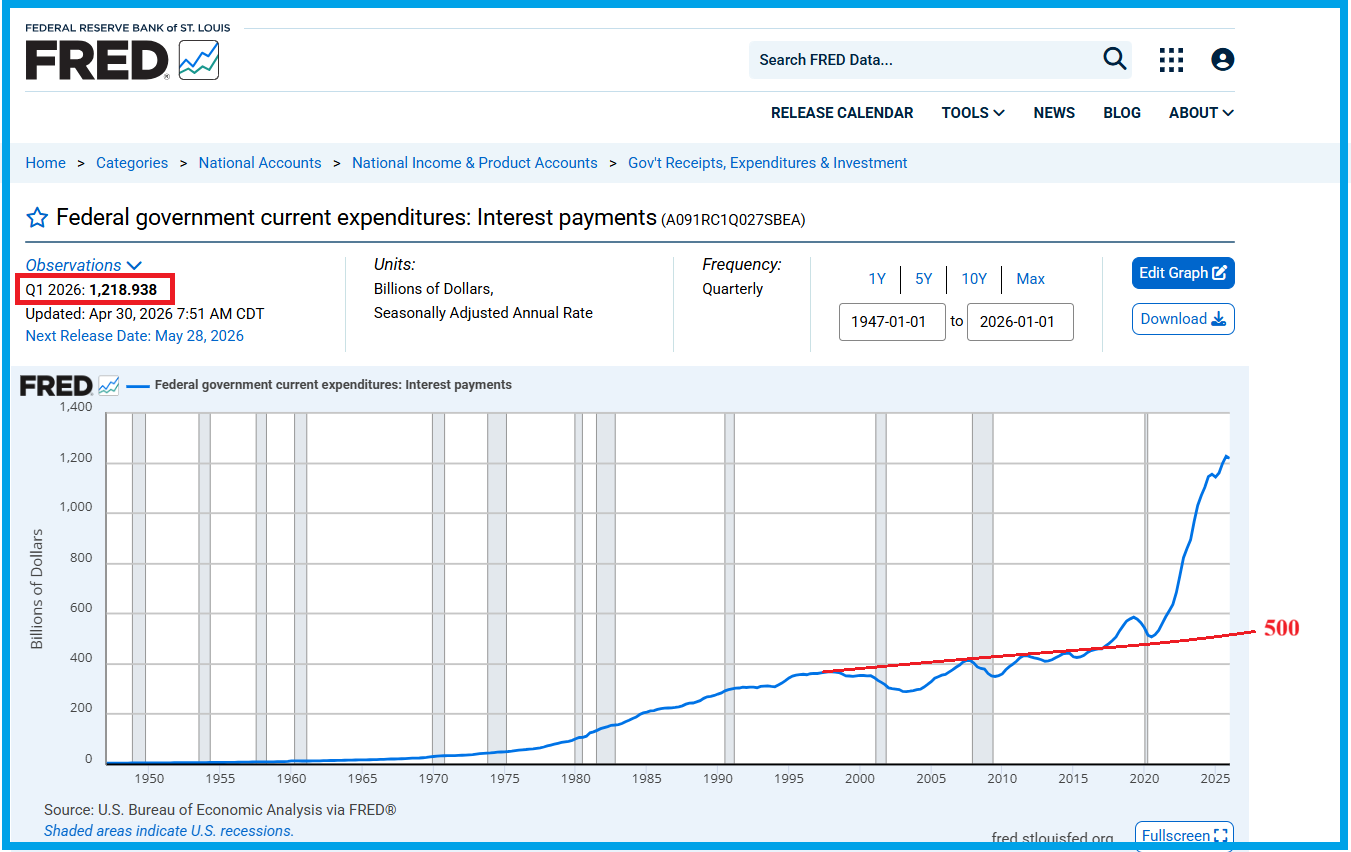

To this end, these manipulators lead everyone to believe that America is on the brink of collapse, particularly due to the federal government’s debt, which is said to far exceed normal levels (reaching 120% of GDP) and is causing interest payments to skyrocket to… $1,219 billion annually by the first quarter of 2026 and… ultimately paid by American taxpayers, as the data published by our friend Fred from St. Louis clearly shows,

Document 2:

However, as I have shown previously, the actual net federal government debt amounts to only 81% of current GDP, which is considered (almost) normal.

The question that then arises is this: why does the federal government’s gross debt generate such high interest payments ($1.219 trillion)?

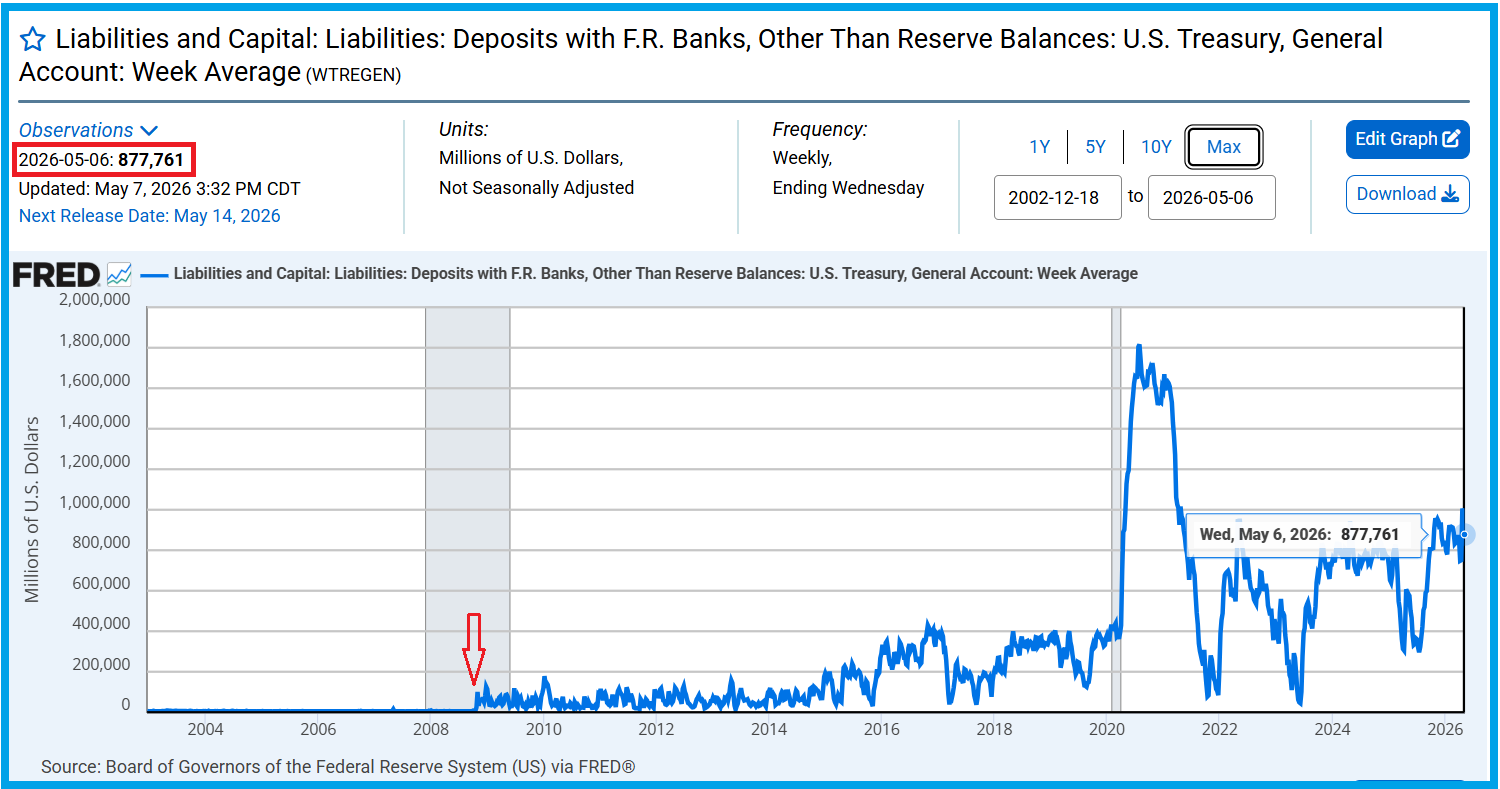

The answer is provided in this chart by our friend Fred from St. Louis: it is because the Treasury’s cash position has become completely out of the ordinary!

Document 3:

In fact, the Treasury’s cash balance was in the range of… 5 to 10 billion dollars only before October 2008, but since October 2023 it has fluctuated within a range of 800 to 1,000 billion dollars, with the exception of a period of a few months in 2025, after peaking at over 1,800 billion dollars in 2021!

By comparison, the overall cash holdings of U.S. companies have increased steadily in line with a consistent upward trend without such sharp spikes, having grown by less than 2.5 times from late 2008 to late 2025,

Document 4:

By comparison and logically, the Treasury’s cash reserves should therefore not currently exceed 25 to 30 billion dollars… whereas they fluctuate within a range of… 800 to 1,000 billion dollars, which obviously contributes to this explosion in interest ultimately paid by American taxpayers!

Furthermore, Ben Bernanke decided to increase the Fed’s purchases of Treasury bonds and mortgage-backed securities (US government securities) starting in 2010 to stimulate growth (QE2), against the advice of, among others, a young Fed governor, namely… Kevin Warsh!

Document 5:

Indeed, a 2010 Wall Street Journal article by Sudeep Reddy explained (among other things) that many Americans, including FOMC members such as Kevin Warsh, were opposed to this monetary policy, which risked reigniting inflation and driving up interest rates,

Document 6:

To boost growth and prevent a rise in rates in the financial markets, Ben Bernanke lowered the Fed’s base rate to its lowest level because it is an administered rate and not determined by free markets, which were then forced to align with the Fed’s zero rate!

Document 7:

Kevin Warsh’s position in 2010 was indeed more logical and consistent than Ben Bernanke’s!

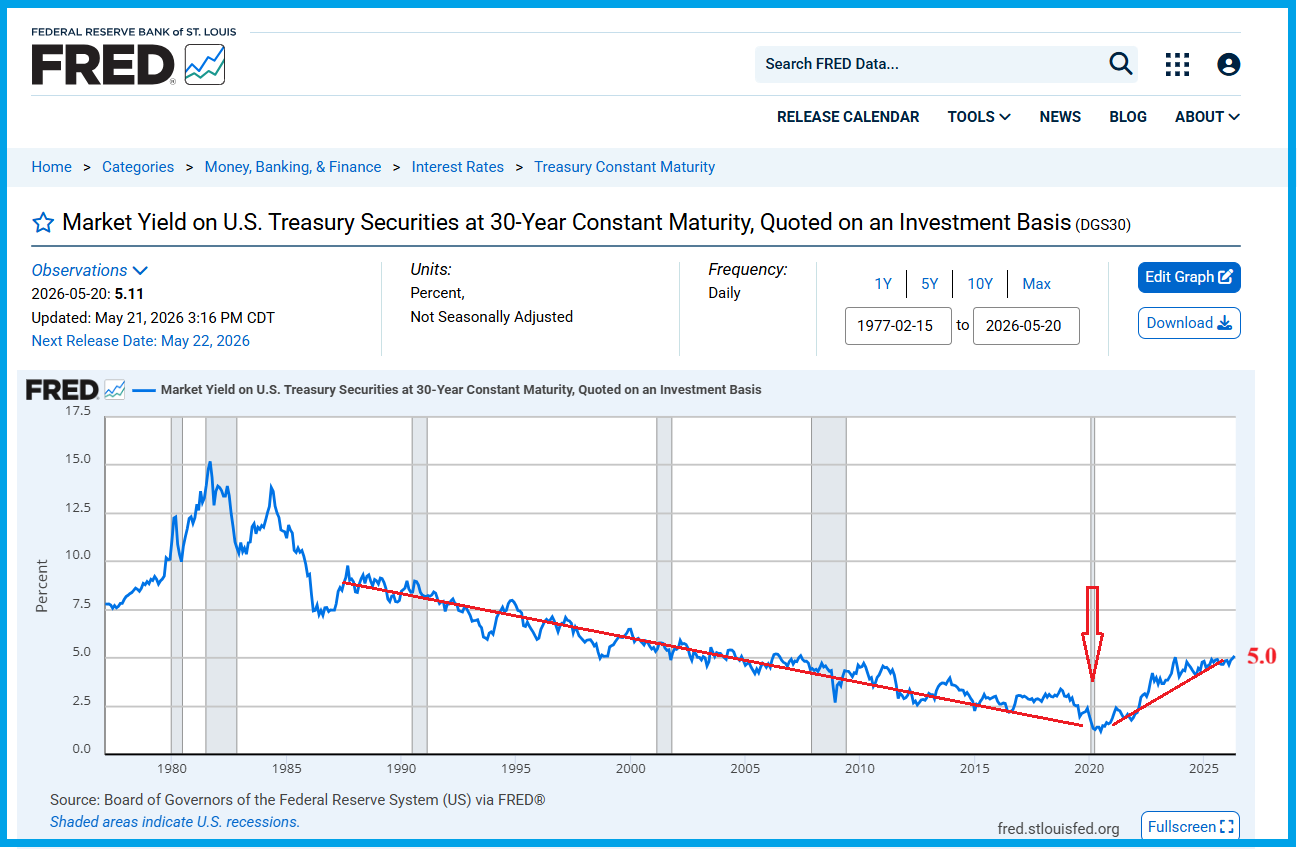

Subsequently, after 2020, as monetary expansion had far exceeded what might have been acceptable limits, some investors began to lose confidence in these securities and became marginal sellers, which drove down contract prices and, conversely, pushed up their yields—including those of the 30-year bond, which under such circumstances serve as a good leading indicator of impending financial turmoil,

Document 8:

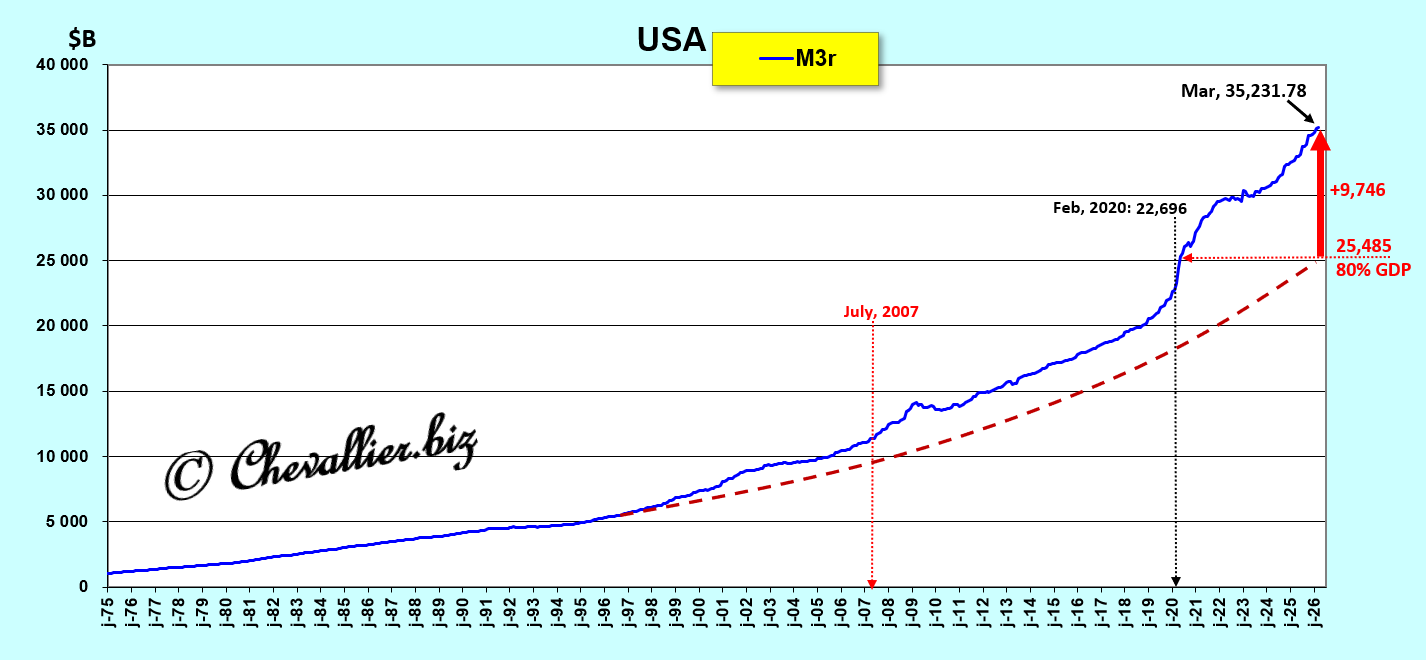

This monetary expansion currently plaguing the United States is currently in the order of… 10,000 billion dollars (see my analyses on this subject)!

Document 9:

However, a simple solution to halt the relative growth of this monetary bubble (relative to GDP) could be to return to a… normal management of the Treasury’s cash reserves, those of government agencies, and the Fed’s assets—as these officials typically did during the second half of the 20th century—by eliminating $11.5 trillion in securities…

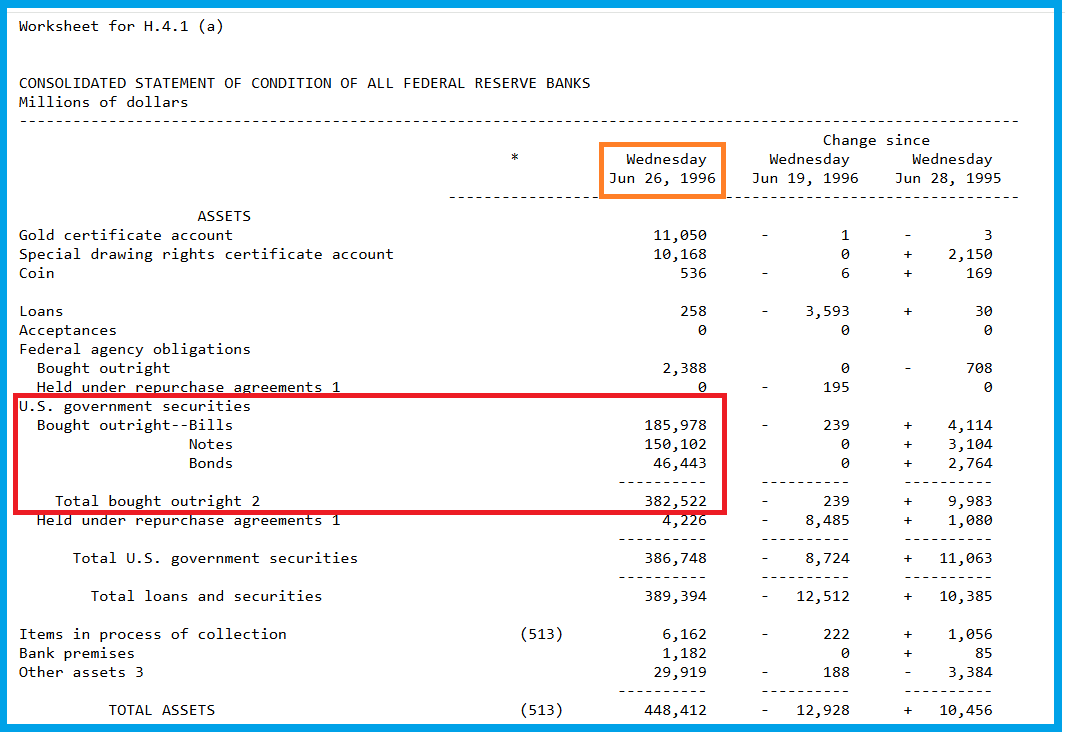

As for the Fed, according to data from its oldest currently available balance sheets dated June 26, 1996, the total U.S. government securities amounted to $382.522 billion, which corresponded to 4.6% of GDP of $8,259.771 billion.

Document 10:

However, this same total of U.S. government securities currently amounts to $4,457.712 billion (see Document 5 above), which corresponds to 14.0% of current GDP of $31,856.257 billion!

To return to a situation equivalent to that of the late 1990s—that is, before the onset of financial and monetarist excesses—the government bonds held by the Fed should logically fluctuate around 1,500 billion dollars only.

Thus, the Fed holds approximately $3 trillion in securities that should not normally be part of its open market policy.

So, to recap, federal agencies have accumulated entirely superfluous gross debt totaling roughly… $11.5 trillion, divided among securities held (in excess) by the Fed ($3 trillion), Intragovernmental Holdings ($7.7 trillion), and the Treasury’s cash (700 billion)!

To provide an accurate picture of reality, the federal government’s gross debt should match its net debt.

To achieve this goal, logically, it would simply be a matter of canceling these debts against itself.

So, while Kevin Warsh was forced to yield to Ben Bernanke in 2010 because the latter was then chairman of the Fed, Kevin Warsh—now having become chairman of the Fed himself—should and could help curb the growth of the monetary bubble that threatens the foundations of U.S. prosperity!

To achieve this goal, he need only drastically reduce the amount of bonds held by the Fed and vigorously urge the Secretary of the Treasury and federal agency leaders to do the same, so as to manage the res publica logically and normally in the interests of American taxpayers, which would allow them to optimize their wealth as well as that of the nation.

Everything is simple said Milton Friedman, provided that… the government is well managed, that is, like a business in a free market where companies always minimize their cash holdings, and the same must therefore apply to federal agencies.

If these $11.5 trillion in government bonds held by federal agencies were completely written off, the total actual federal government debt would drop from $39 trillion to $27.5 trillion ($39 trillion – $11.5 trillion), which would have two major consequences…

First, the interest paid by taxpayers would no longer be 1,219 billion dollars (see Document 2 above) but in the range of… 500 billion dollars (on an annual basis) and even less thanks to lower interest rates…

Second, in fact, once fewer Treasury bills are in circulation, bond prices would rise and, conversely, their yields would fall, all other things being equal.

There would then be both less debt and lower rates, so the interest paid by U.S. taxpayers would amount to only around $400 billion, which would leave them with… an additional $800 billion (over a year) compared to the current situation!

Put another way: the mismanagement of the res publica deprives American taxpayers—both individuals and corporations—of 800 billion dollars a year!

Conclusion: Kevin Warsh should therefore reduce the stock of government bonds held by federal organizations to a minimum, which should stimulate growth and investment, thereby increasing the creation of wealth for Americans.

Unfortunately, these measures would not be enough to burst the monetary bubble plaguing the United States, as these government bonds held by federal agencies are not part of the money supply.

However, a return to sound management of the res publica and this $800 billion injection stimulating growth could encourage capital holders to withdraw their funds from money market mutual funds and invest them in wealth-creating assets.

For example, Warren Buffett’s Berkshire Hathaway currently holds… $400 billion in cash reserves that do not generate wealth! A return to sound fundamentals would encourage the company to invest this money instead of financing… this public debt, whose disadvantages outweigh its benefits.

Furthermore, a return to growth on a sound footing would lead corporate executives to invest more rather than hoard cash flows that are growing too rapidly—see my article on the money supply.

Indeed, following the spike caused by this coronavirus situation, the increase in monetary bloat is primarily due to the M3-M2 monetary aggregate, which consists of total corporate cash and deposits in money market funds.

Thus, Kevin Warsh could put an end to the expansion of the monetary bubble that fundamentally hampers the U.S. economy without, however, managing to burst it in a way that would return to a normal situation—that is, with an M3 money supply ratio below 80% of current GDP, as was the case during the second half of the 20th century (see Document 1 above).

There is therefore no conceivable solution to put an end to this excessive growth of the money supply in the United States, and it is this that is fundamentally causing the end of America’s global leadership.

This loss of America’s omnipotence is not caused by the size of the federal government’s debt, nor by corporate or household debt, nor by deindustrialization, nor by the excessive financialization of economic activities, nor by wokism, nor by anything else…

The first pillar of Reaganomics is a sound currency, according to Arthur Laffer.

During the second half of the 20th century, FOMC members could always lower one of the three monetary aggregates by triggering a recession, which consistently kept the M3 money supply below the critical threshold of 80% of GDP.

To achieve this goal, all they had to do was raise the Fed’s base rate to trigger a recession.

This is what allowed the M3/GDP ratio to be kept within the critical 80% limit, but it is no longer possible in the 21st century because this monetary bubble has grown too large.

The only conceivable solution to burst this monetary bubble would be for the globalists to create a major crisis—a collapse of economic activity unlike anything ever seen in the United States, a Great Reset as some networks have suggested—but they lack the ability to implement it in the foreseeable future, and that is fortunate, as such a situation would have catastrophic consequences.

The Americans are therefore victims of their own mistakes and of having abandoned their monetarist culture, even as they were convinced they could continue to exercise their leadership over the world forever.

It is now China that has become the world’s greatest power, largely thanks to Deng Xiaoping, who succeeded in convincing the ruling (Communist) Party to abandon… communism and adopt liberal capitalism.

Moreover, China’s leaders have become the staunchest defenders of this liberal capitalism, which is based, of course, on freedom, while U.S. leaders resort to and abuse threats, sanctions, coercion, predation, and wars.

***

Click here to read Sudeep Reddy’s article published in the Wall Street Journal in 2010.

Click here to access the Fed’s page publishing its balance sheet as of June 27, 1996.

© Chevallier.biz